Dis-equilibrated Markets

The static benefits of markets all come from markets being in equilibrium (class 3.3):

- allocative efficiency (CS+PS)

- Pareto efficiency

- productive efficiency

But don’t forget the dynamic benefits of markets as a discovery process! (class 3.4)

- discovery of better allocations of resources

- creation & elimination of profit opportunities

- entrepreneurship & innovation

Dis-equilibrated Markets

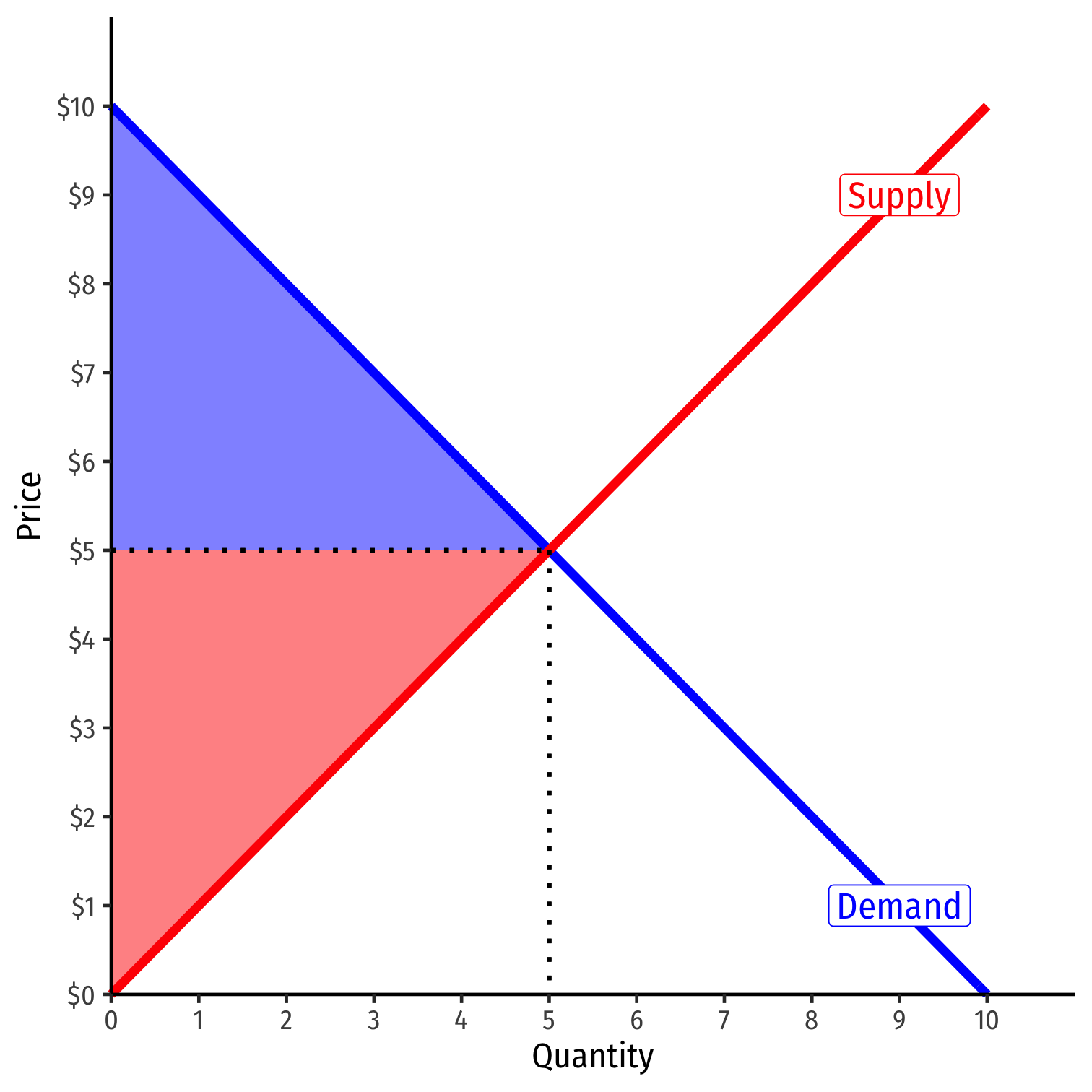

To reach equilibrium, market prices need to be able to adjust

- Shortage: price needs to rise

- Surplus: price needs to fall

There are unrealized gains from trade that exist in disequilibrium (shaded)

- Buyers & sellers both can be made better off if they can adjust the price

Dis-equilibrated Markets

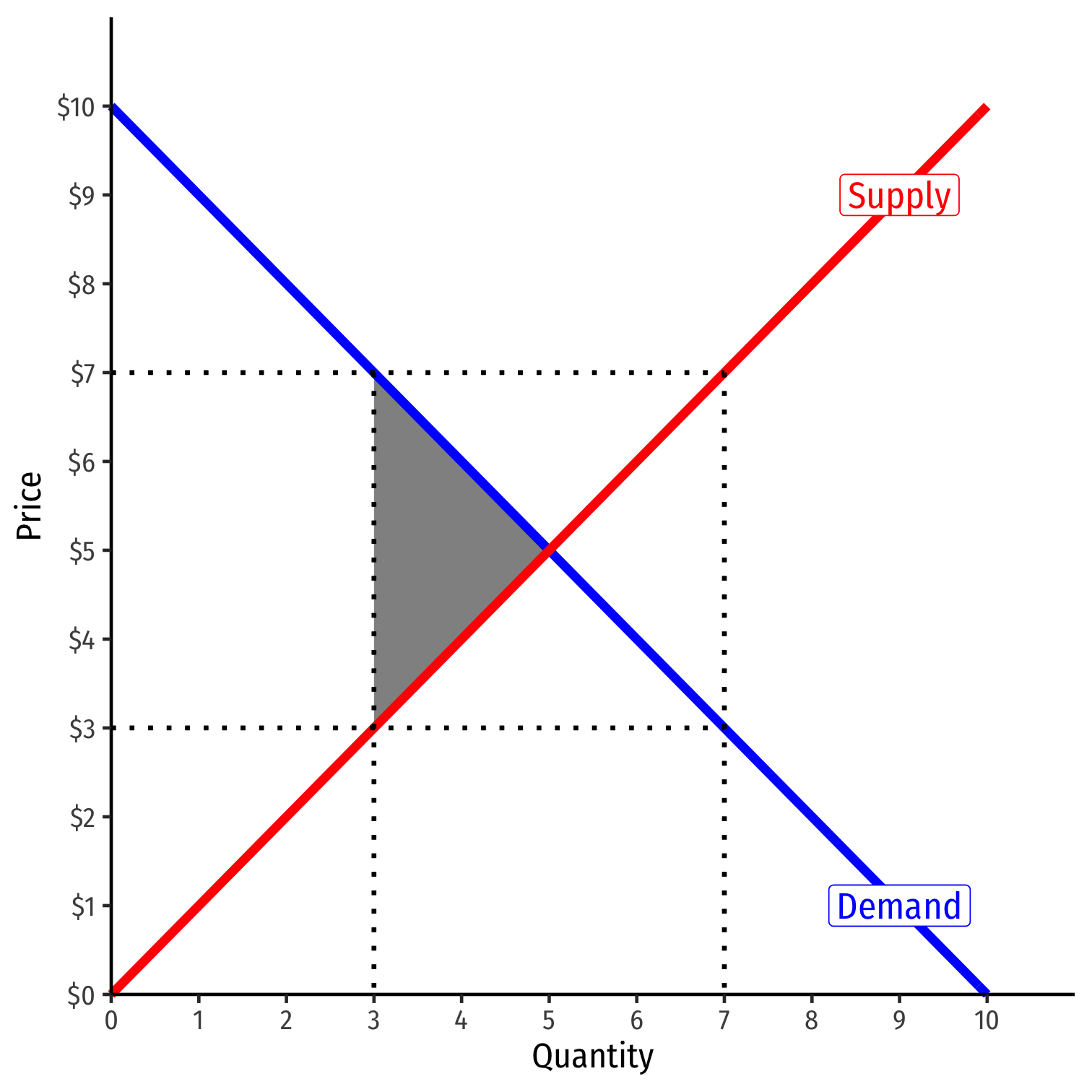

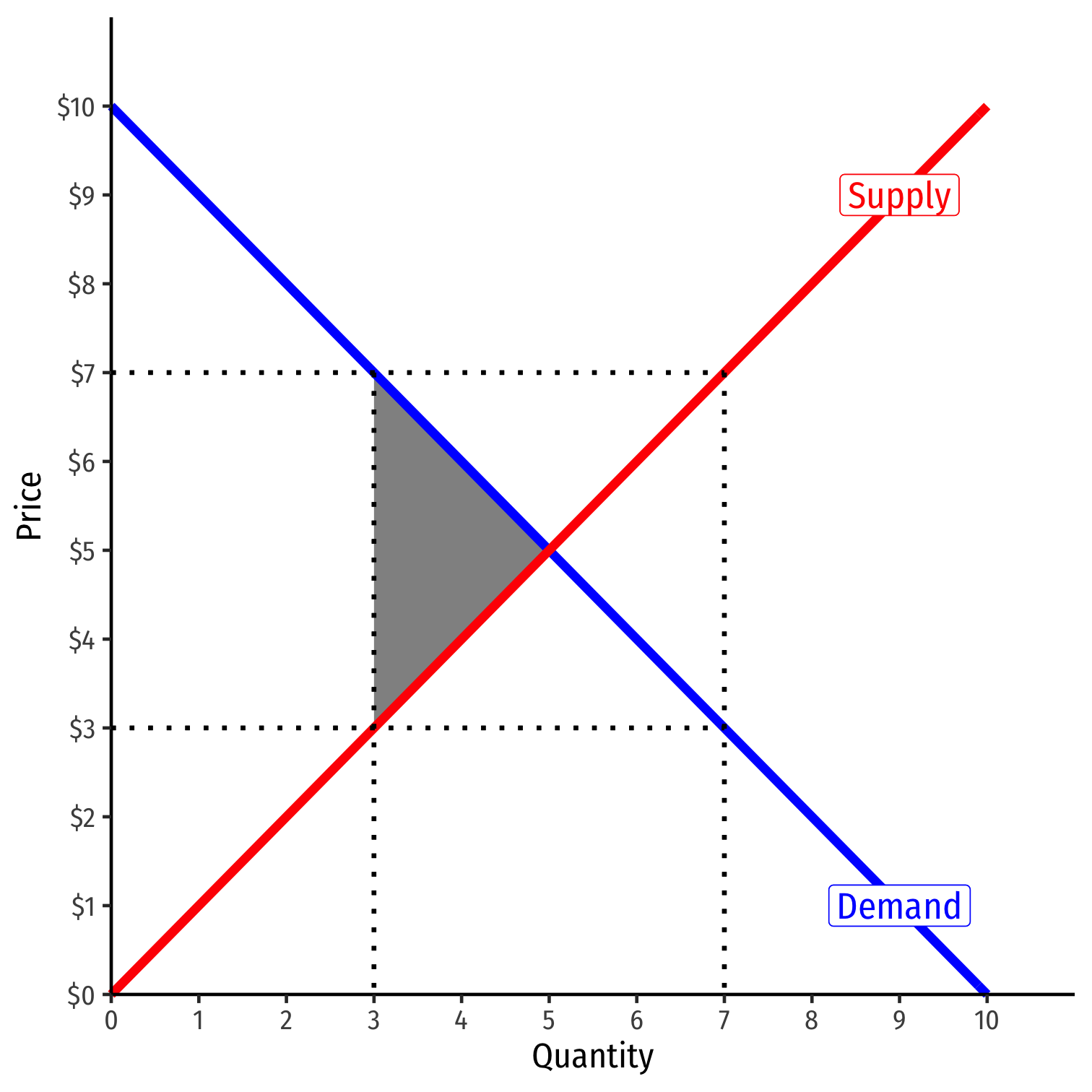

If market prices are prevented from adjusting, shortage/surplus becomes permanent

Lost CS and/or PS: Deadweight loss (DWL)

- inefficiency created by (permanent) diseq.

Various government policies can prevent markets from equilibrating & create DWL:

- Price regulations (price ceiling like rent control, price floor like minimum wage)

- Taxes, subsidies, tariffs, quotas†

- These should have been covered in Principles (see my slides on taxation from ECON 410)

† Some may be necessary (taxes fund government), but create market inefficiencies.

An Example: Some Economic Impacts of Covid

The toilet paper aisle of my Giant grocery store, March 2020

Where did all of the ... go?

- Toilet paper

- Hand sanitizer

- Masks

- PPE

- Ventilators

Three major issues:

- price elasticity of supply

- price gouging laws

- restrictions & regulations on supply

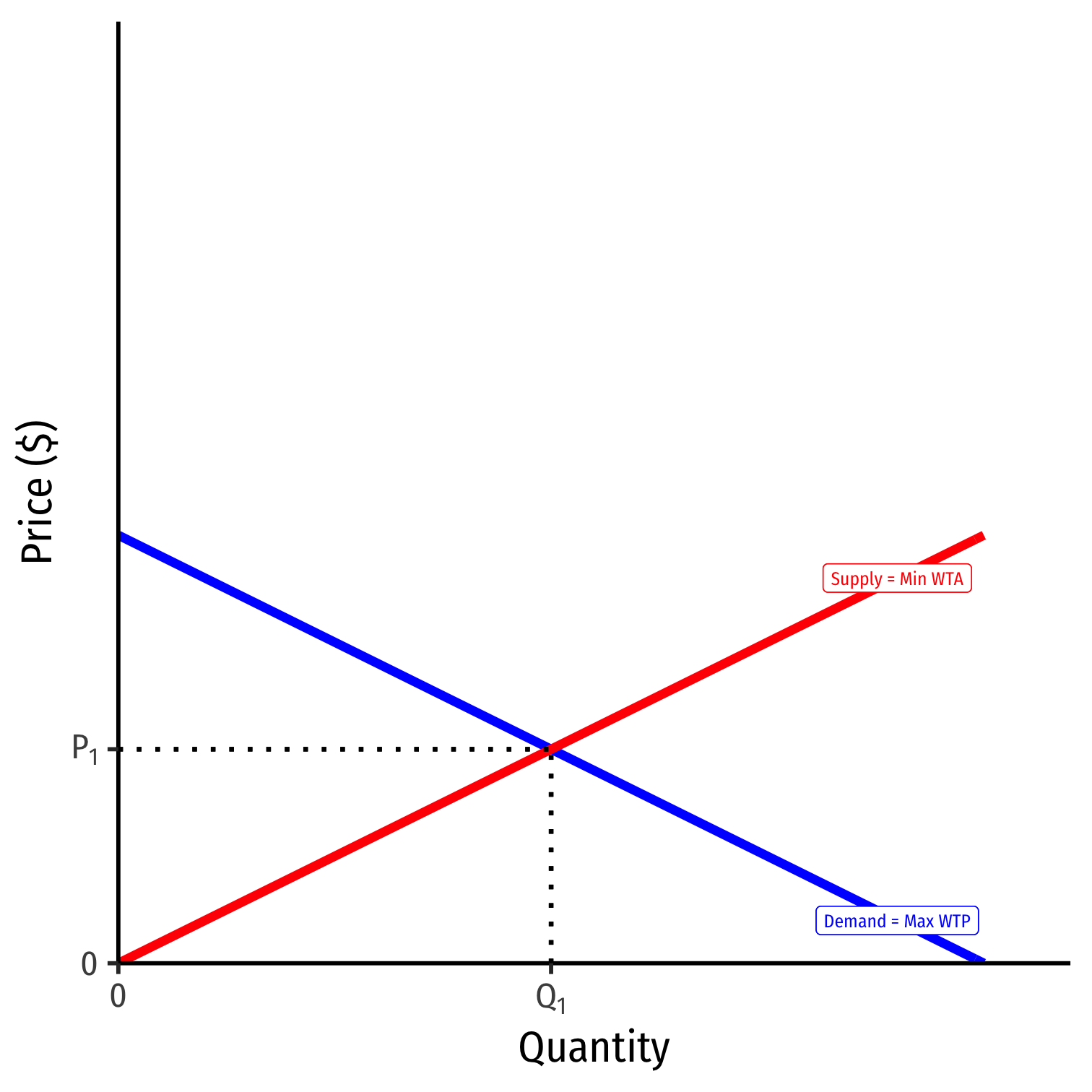

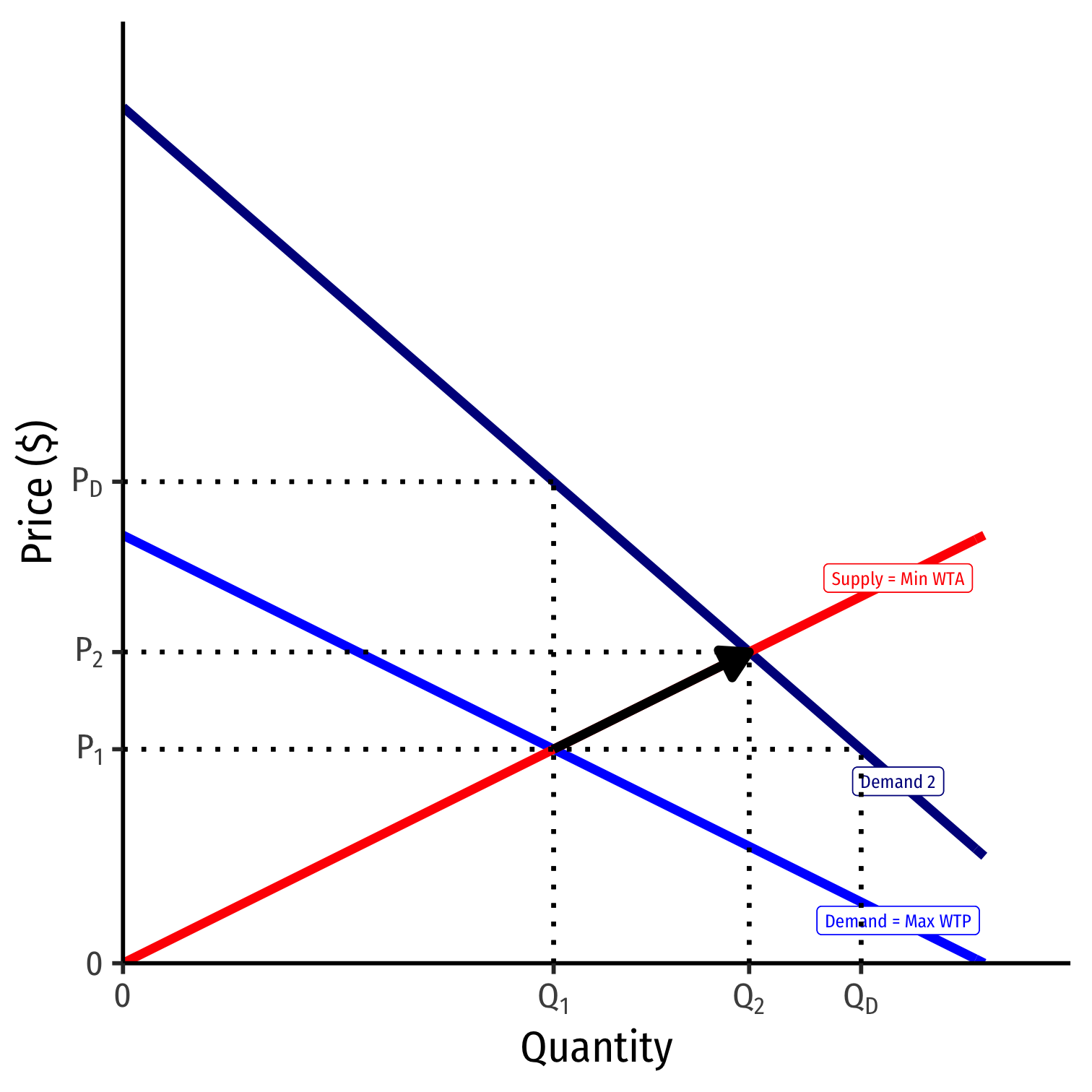

Increase in Demand

- Consider a market for a good in equilibrium, P1

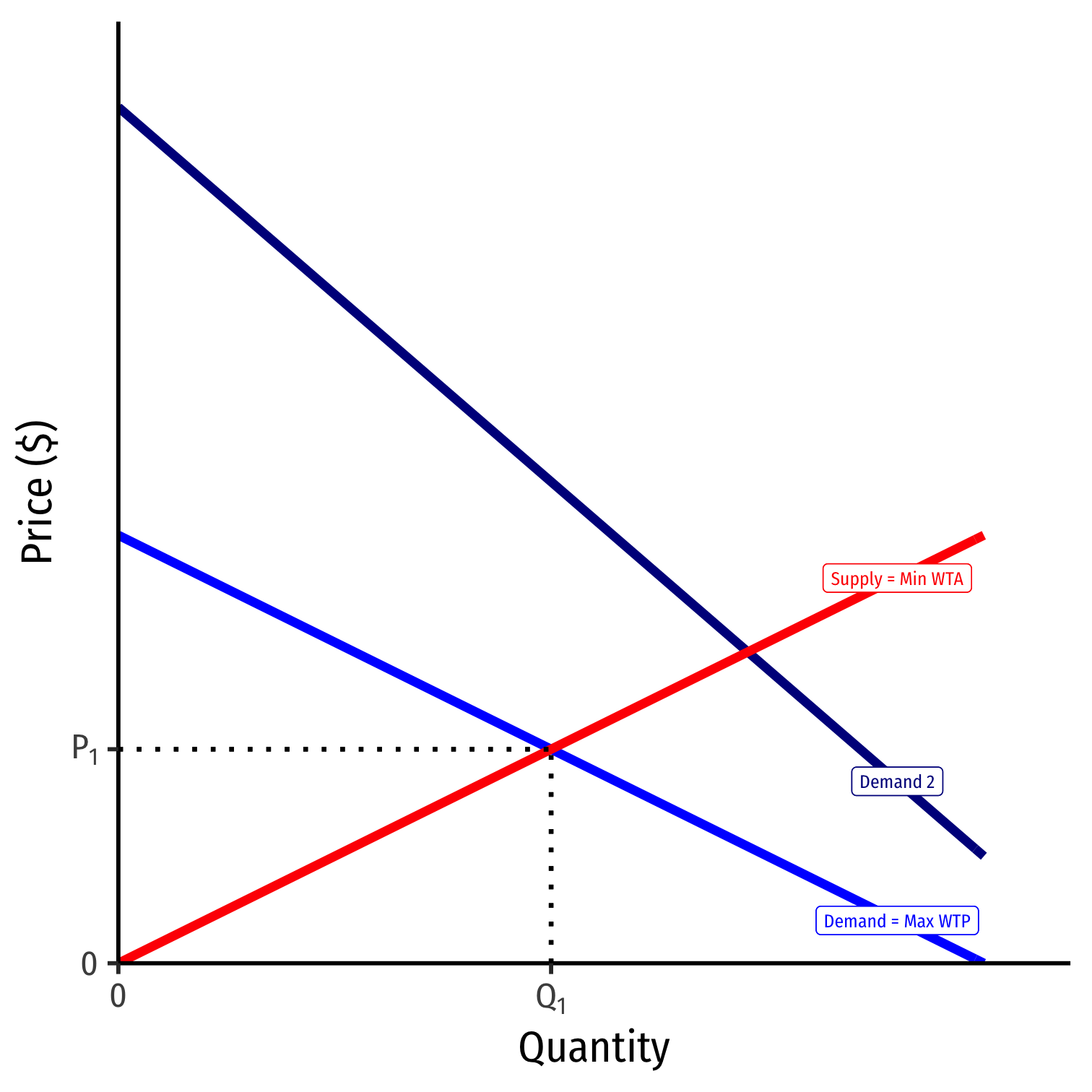

Increase in Demand

More individuals want to buy more of the good at every price

Demand increases, becomes less elastic

Increase in Demand

More individuals want to buy more of the good at every price

Demand increases, becomes less elastic

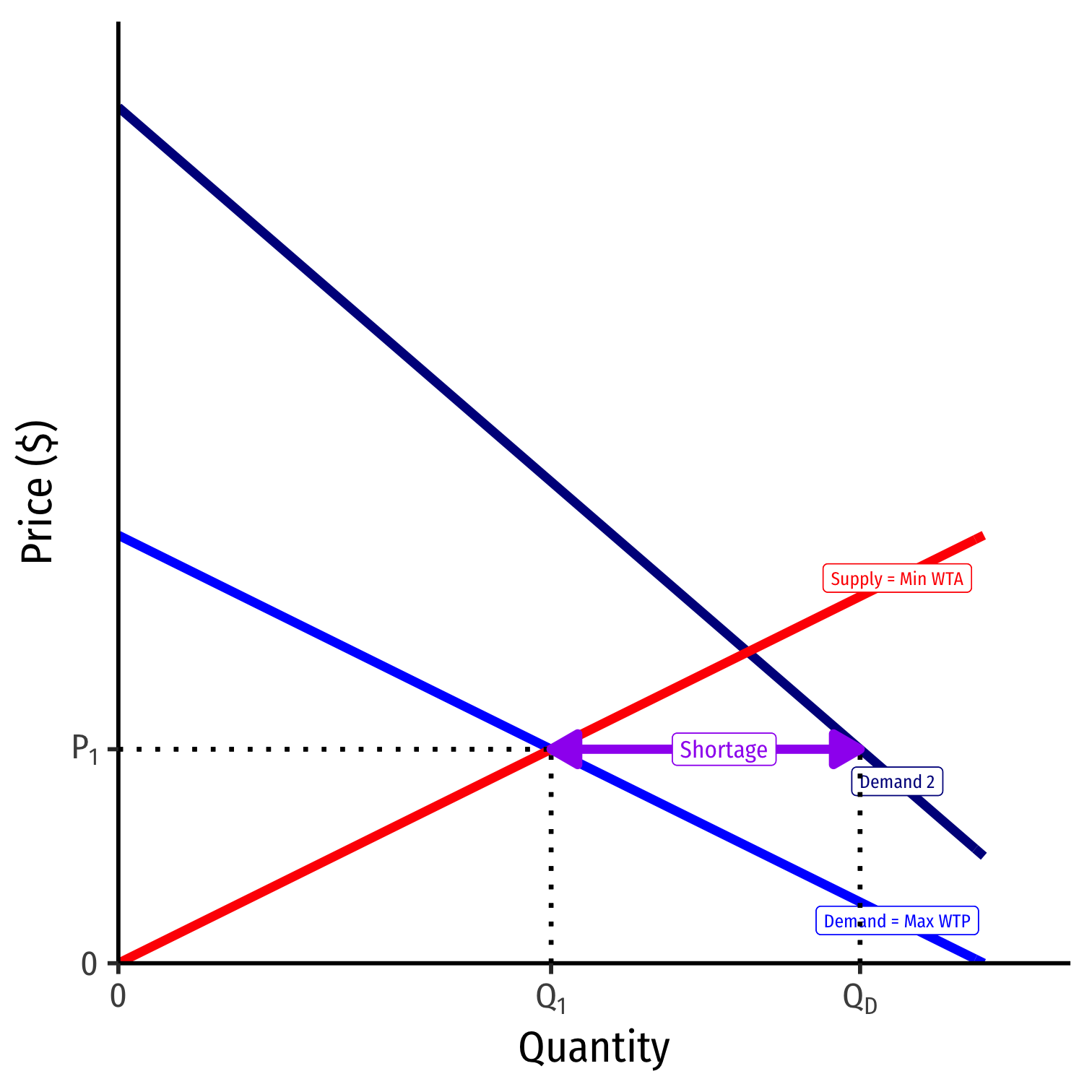

At the original market price, a shortage! (qD>qS)

Increase in Demand

More individuals want to buy more of the good at every price

Demand increases, becomes less elastic

At the original market price, a shortage! (qD>qS)

Sellers are supplying Q1, but some buyers willing to pay more for Q1

Increase in Demand

More individuals want to buy more of the good at every price

Demand increases, becomes less elastic

At the original market price, a shortage! (qD>qS)

Sellers are supplying Q1, but some buyers willing to pay more for Q1

Buyers raise bids, inducing sellers to sell more

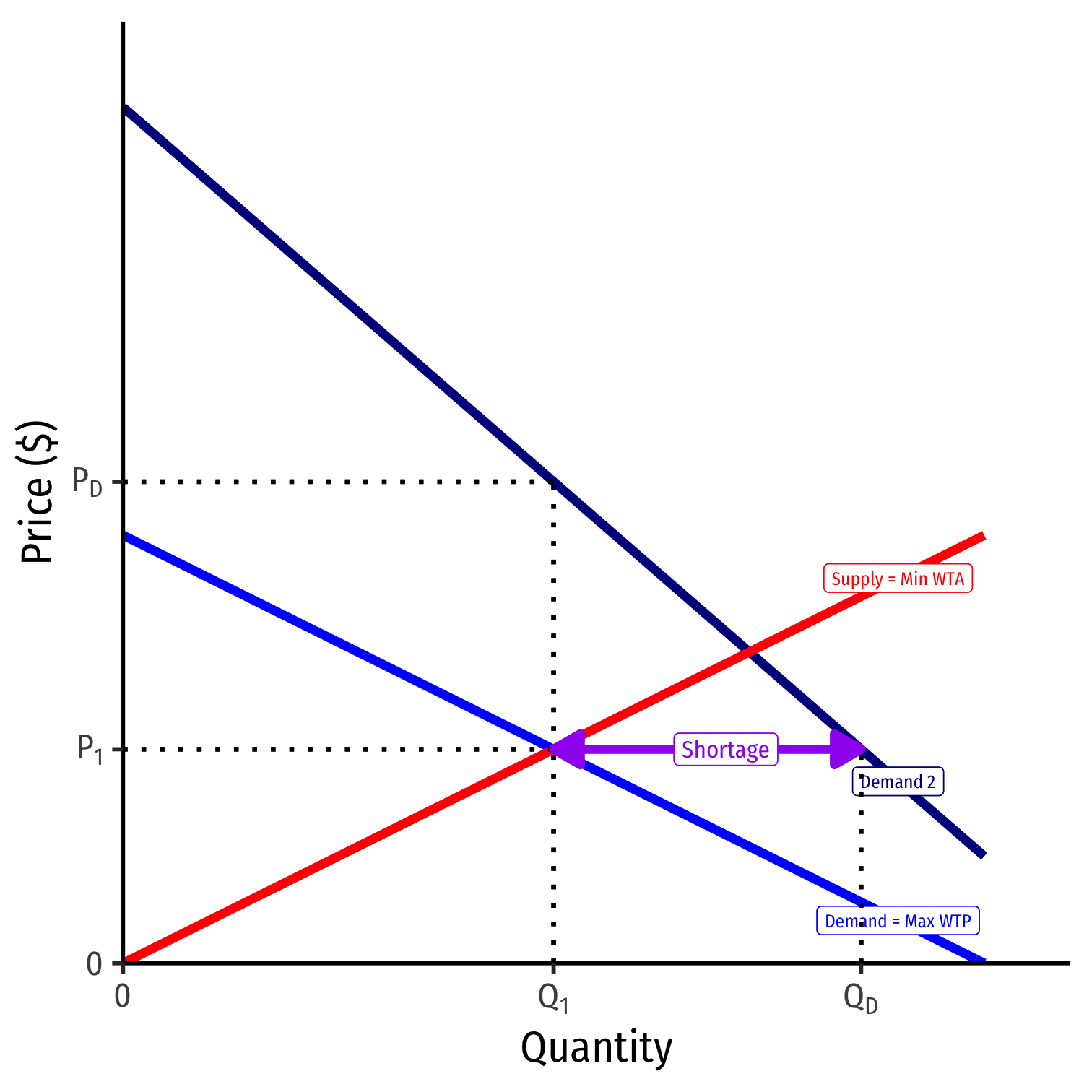

Reach new equilibrium with:

- higher market-clearing price (P2)

- larger market-clearing q. exchanged (Q2)

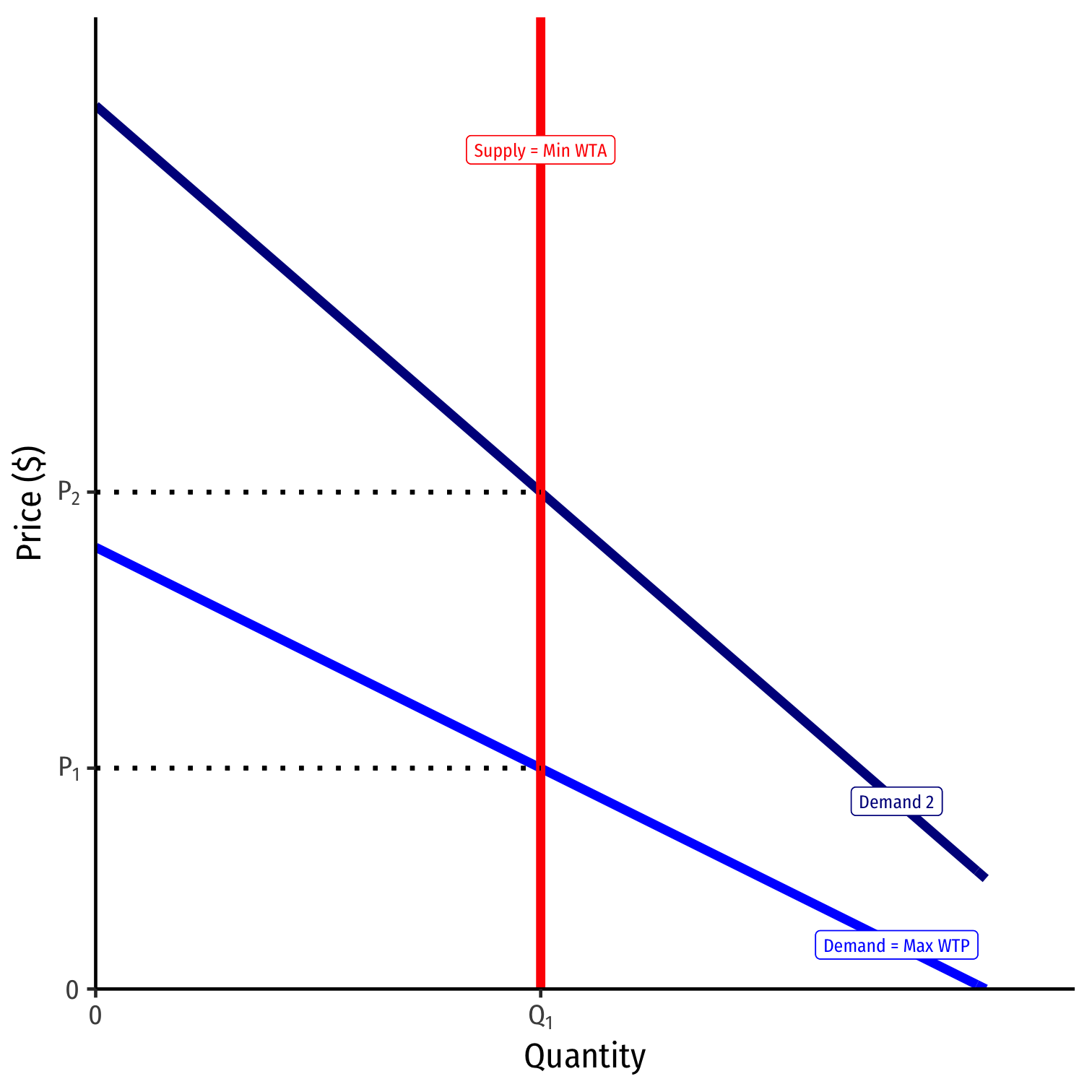

One Possibility: Inelastic Supply

It might that supply is very inelastic

- Here: perfectly inelastic (for convenience)

Suppliers can’t produce and sell more units even if they want to at very high price demanded

- sudden shock to inventories (short run)

- rising production costs

- government regulations & restrictions

Thus, the new high price is an equilibrium that will persist for a while

- no “inefficiency,” just a fixed supply of goods we cannot easily change

One Possibility: Inelastic Supply

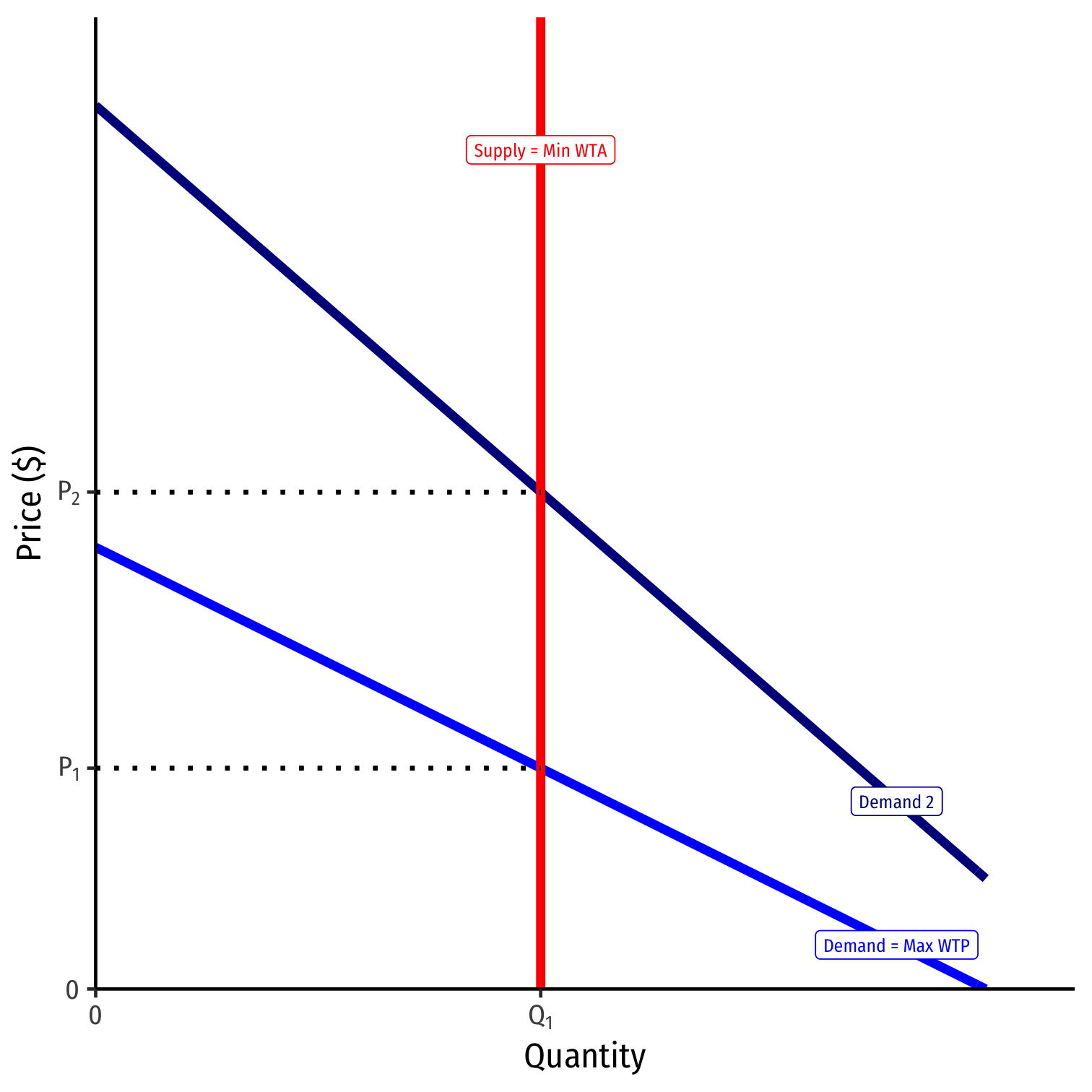

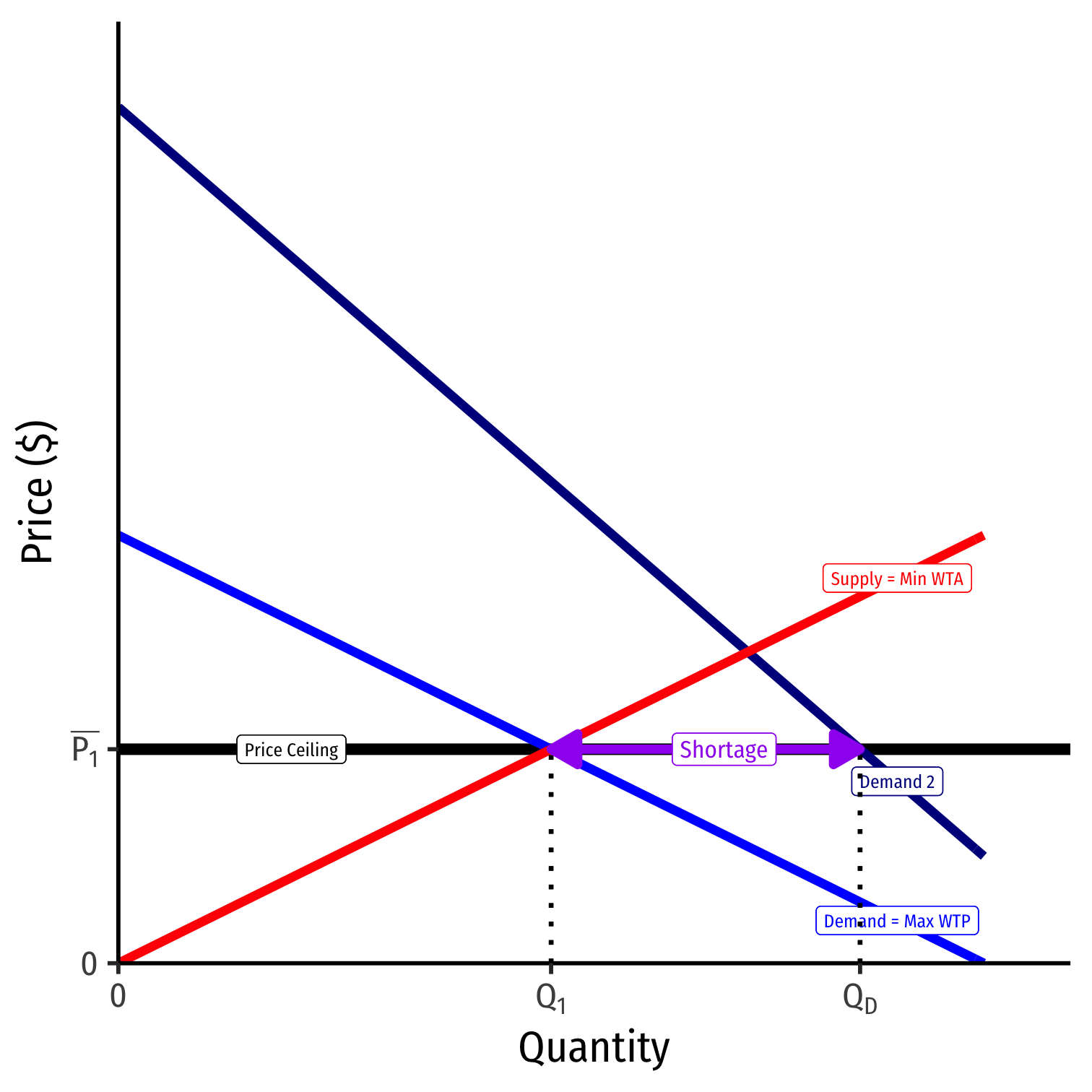

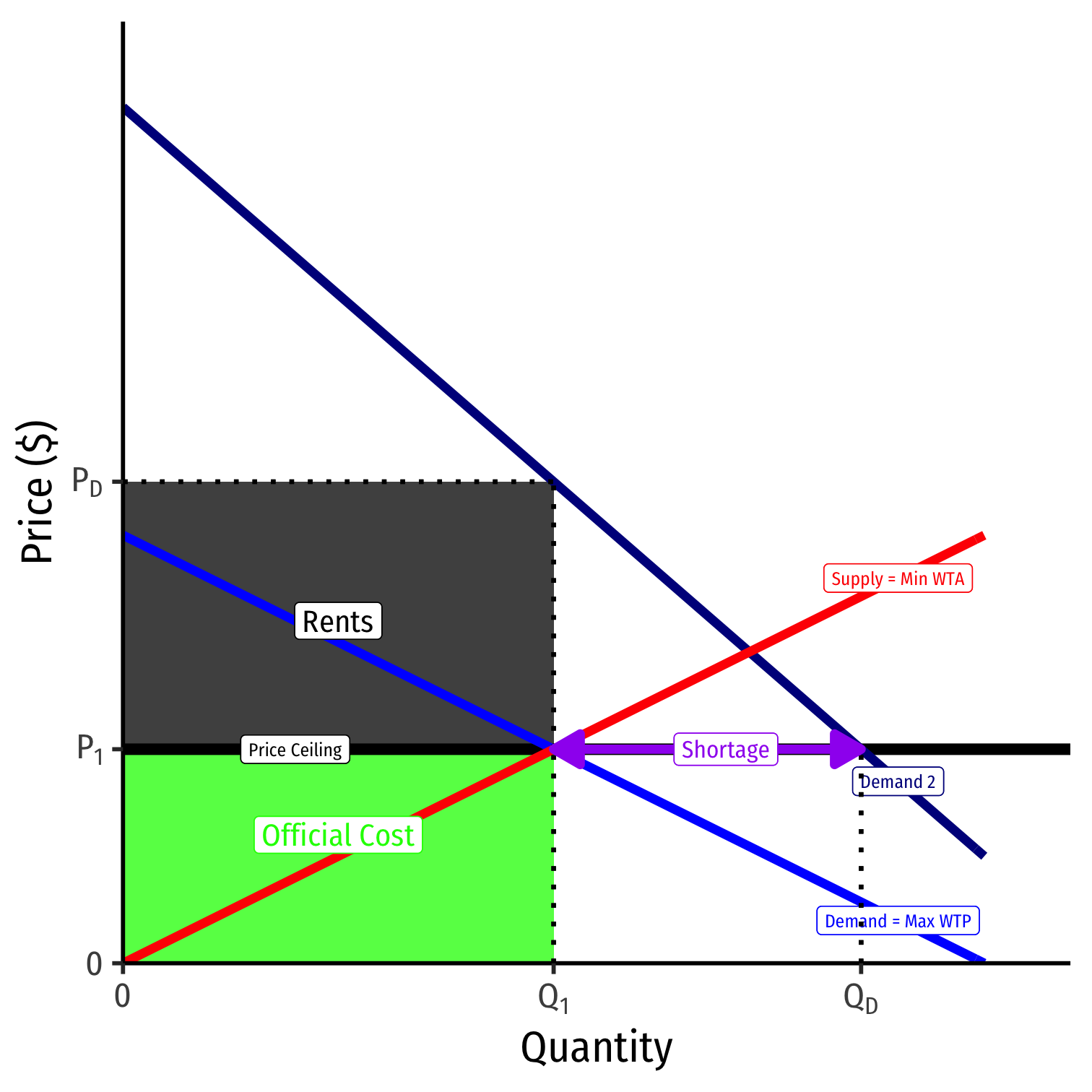

Price Gouging Laws

Additionally, government has anti-price-gouging laws, a price ceiling at the original price, P1

Qd>Qs: excess demand, a shortage!

Sellers will not supply more than Q1 at price ¯P1

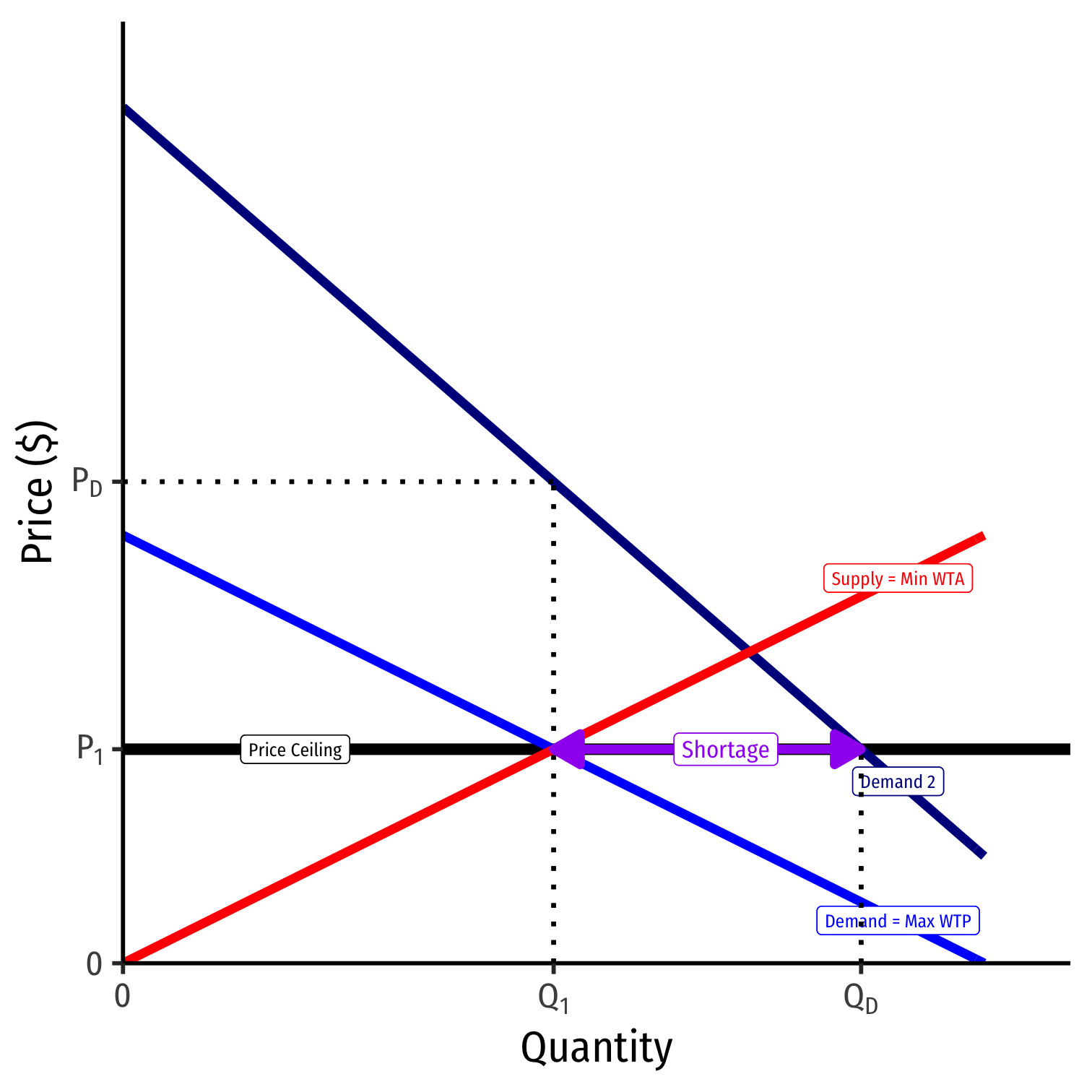

Price Gouging Laws

Additionally, government has anti-price-gouging laws, a price ceiling at the original price, P1

Qd>Qs: excess demand, a shortage!

Sellers will not supply more than Q1 at price ¯P1

For Q1 units, buyers are willing to pay PD!

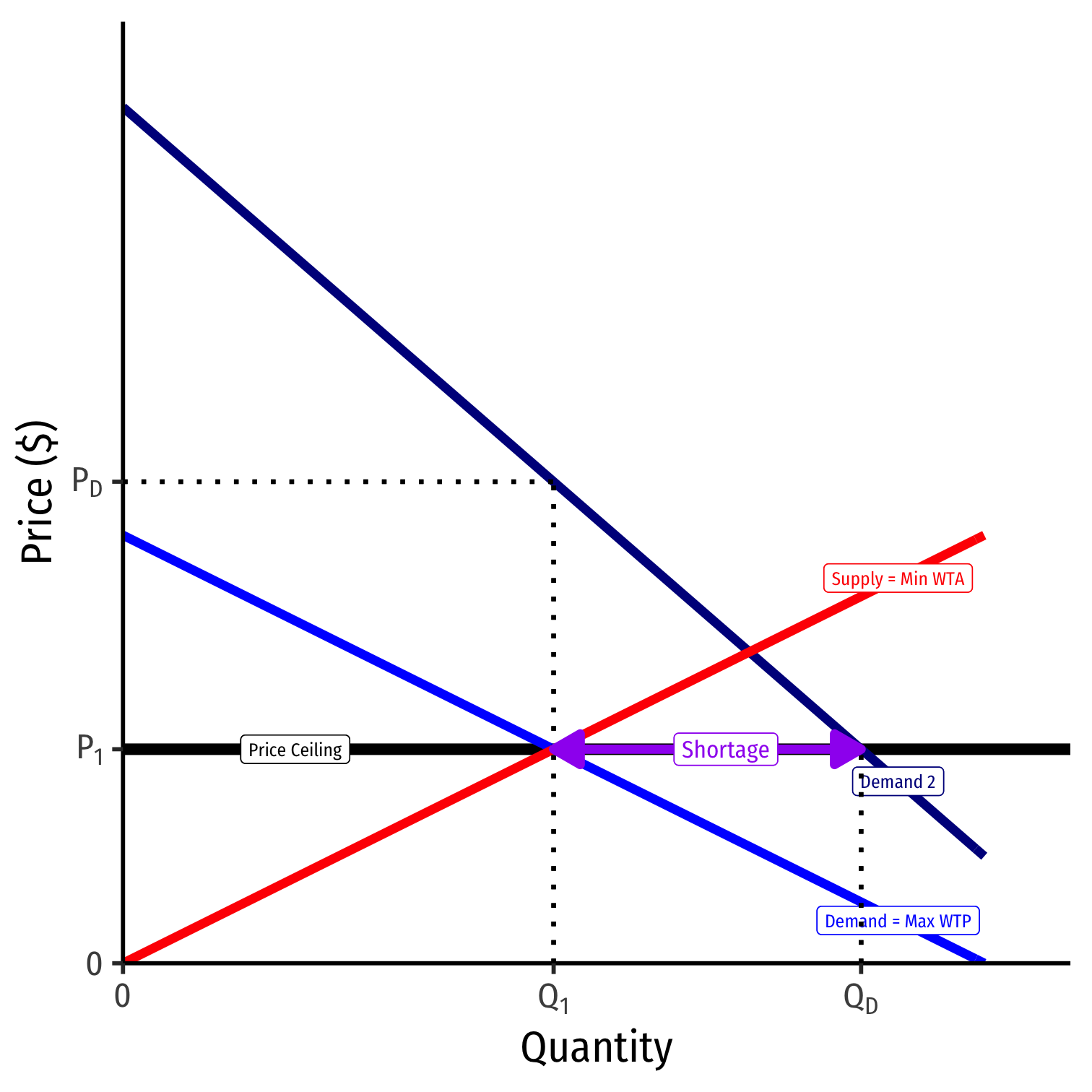

Price Gouging Laws

If prices were allowed to adjust: buyers would bid higher prices to get the scarce Qs goods

Sellers would respond to rising willingness to pay, and produce and sell more

But the price is not allowed to rise above ¯P1!

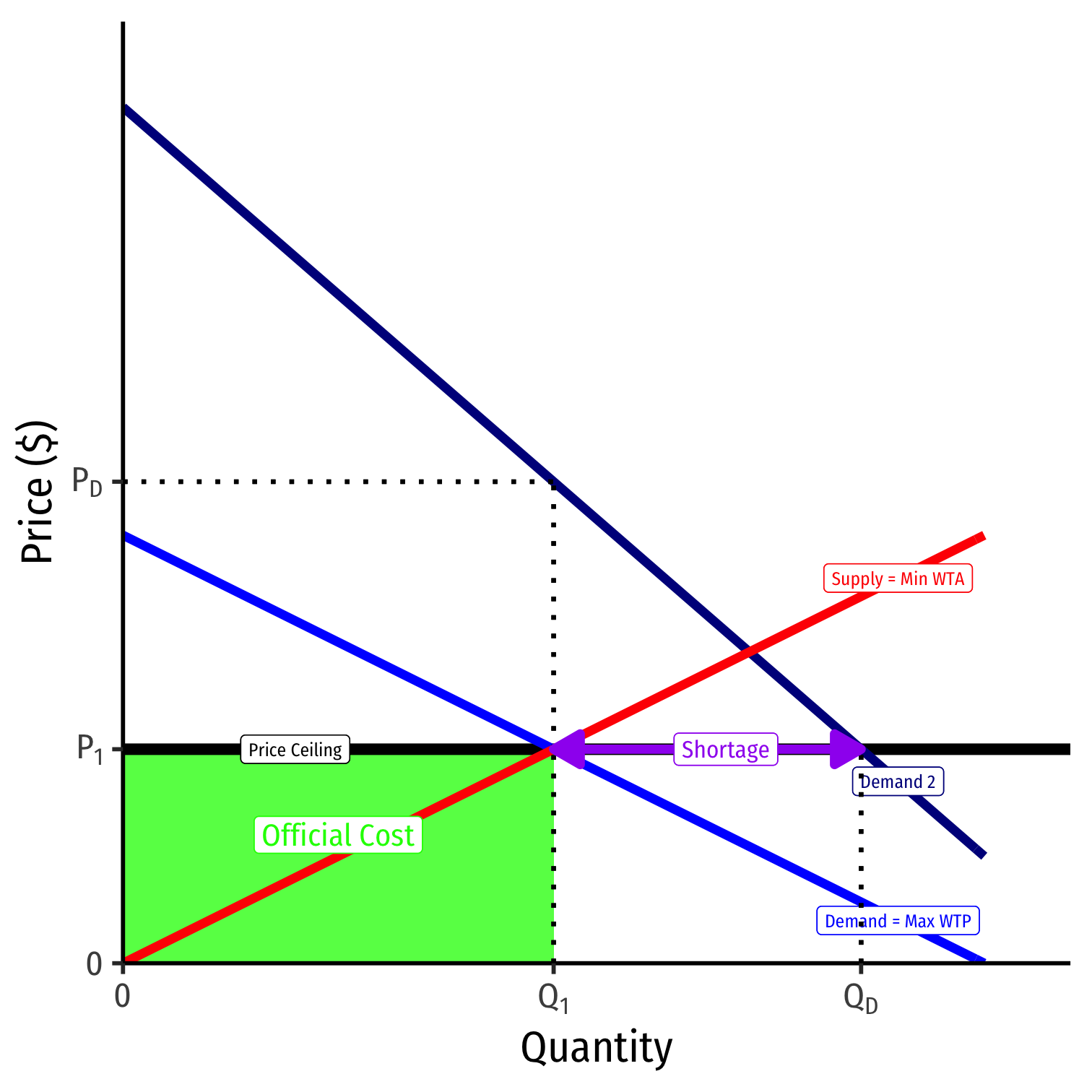

Price Gouging Laws

- Official price is P1, sellers gain monetary revenues

Price Gouging Laws

Official price is P1, sellers gain monetary revenues

Competition exists between buyers to obtain scarce Qs goods

- Buyers willing to pay PD unofficially

Goods are distributed by non-market means:

- Queuing

- Black markets

- Political connections, favors, corruption

Economic rents: excess resturns (above cost) go to those who own & distribute the scarce goods

Forms of Rents

(Temporarily) Raising Prices Can Solve the Shortage

A relatively high price:

Conveys information: good is relatively scarce

Creates incentives for:

- Buyers: conserve use of this good, seek substitites

- Sellers: produce more of this good

- Entrepreneurs: find substitutes and innovations to satisfy this unmet need

(Temporarily) Raising Prices Can Solve the Shortage

"The Canadian National Post, citing the Canadian Food Inspection Agency, says that 'There are no shortages or disruptions to [food] production, importation or export,' and that 'the shelves remain stocked.' ... 'A price surge as a result of natural market forces is not something that is regulated by Canadian competition laws or otherwise. Canada’s competition laws generally don’t interfere with the free market.' ... Canadians will have enough food to eat. But it will be more expensive.

Forcing Low Prices Doesn't Solve the Shortage

U.S. Representative inadvertently makes the case for “price gouging”

Supply-Side Restrictions & Regulatory Burden

"As the nation’s economy and health-care system struggle to adjust to the pandemic, more and more states are reexamining some of their oldest occupational and business regulations—rules that, although couched as protecting consumers, do far more to limit competition...While some states have ordered their occupational-licensing boards to speed up the licensure of new health-care practitioners, others...are granting immediate licensing reciprocity to any practitioner licensed in any state...Even Florida, which has long jealously guarded its occupational-licensing regime to prevent semiretired snowbirds from poaching on the locals’ turf, [is] allowing out-of-state health-care providers to practice telemedicine in the state without a license."

Supply-Side Restrictions & Regulatory Burden

"Illinois has waived licensure fees for retired medical practitioners who wish to resume practice. Oklahoma and Massachusetts have eliminated restrictions that required doctors to have a preexisting doctor-patient relationship before they could offer telemedicine services."

Supply-Side Restrictions & Regulatory Burden

"Also being reexamined are state certificate-of-need, or CON, laws. A product of 1970s-era economic regulation, CON laws require health-care providers to prove that new services are “needed” before they may purchase certain large equipment, open new or expanded facilities, or—as is crucial now—offer home health-care services. Often, these laws give an effective veto power to existing medical providers, allowing them to torpedo new competition for their own benefit...Basic economics predicts that competition reduces prices for consumers, and occupational licensing works directly to stifle competition."

Supply-Side Restrictions & Regulatory Burden

"The University of Minnesota economist Morris Kleiner, a leading researcher on occupational licensing, estimates that licensing costs consumers nearly $200 billion annually. This might be justifiable if licensing produced substantial improvements in quality, yet most research has failed to find a connection between licensure and service quality or safety."

Supply-Side Restrictions & Regulatory Burden

Supply-Side Restrictions & Regulatory Burden

Supply-Side Restrictions & Regulatory Burden

Supply-Side Restrictions & Regulatory Burden

How did the U.S. government only manage to produce a fraction as many testing kits as its peer countries? There have been three major regulatory barriers so far to scaling up testing by public labs and private companies: 1) obtaining an Emergency Use Authorization (EUA); 2) being certified to perform high-complexity testing consistent with requirements under Clinical Laboratory Improvement Amendments (CLIA);...

Supply-Side Restrictions & Regulatory Burden

...and 3) complying with the Health Insurance Portability and Accountability Act (HIPAA) Privacy Rule and the Common Rule related to the protection of human research subjects. On the demand side, narrow restrictions on who qualified for testing prevented the U.S. from adequately using what capacity it did have.

Economic Theory Assumes Good Institutions

Markets & price theory: how consumers & producers specialize, produce, & exchange within given, well-functioning markets (& politics)

Assumes existence of "good" economic & political institutions that facilitate market exchange

- low transaction costs

- clear and enforced property rights

- rule of law

- contract enforcement

- capable, high-capacity, non-corrupt government

- dispute resolution

- high level of social trust

Robust Political Economy

No system is perfect

We need to find arrangements that are robust to knowledge & incentive problems

Easy (unpersuasive) case: perfect information & pure benevolence

- every system works in theory!

Hard (persuasive) case: uncertainty & selfish behavior

- what works best in practice?

Treat people as they are: sometimes good, bad, smart, stupid, opportunistic, altruistic, depending on the institutions they face!

Robust Political Economy

Robust Political Economy

People often recommend optimal policies as if they could be installed by a benevolent dictator

- A dispassionate ruler with total control, perfect information, and selfless incentives to implement optimal policy

- A “1st-best solution”

In reality, 1st-best policies are distorted by the knowledge problem, the incentives problem, and politics

- Real world: 2nd-to-nth-best outcomes

Comparative Institutional Analysis

Compare imperfections of feasible and relevant alternative systems

- The “Nirvana Fallacy”: comparing an imperfect system in reality with an ideal system in theory

Economics: think on the margin!

- One system's “failure” does not automatically imply another will be “successful”!

- Real world requires tradeoffs

- “economics puts parameters on people's utopias”

- “compared to what?”

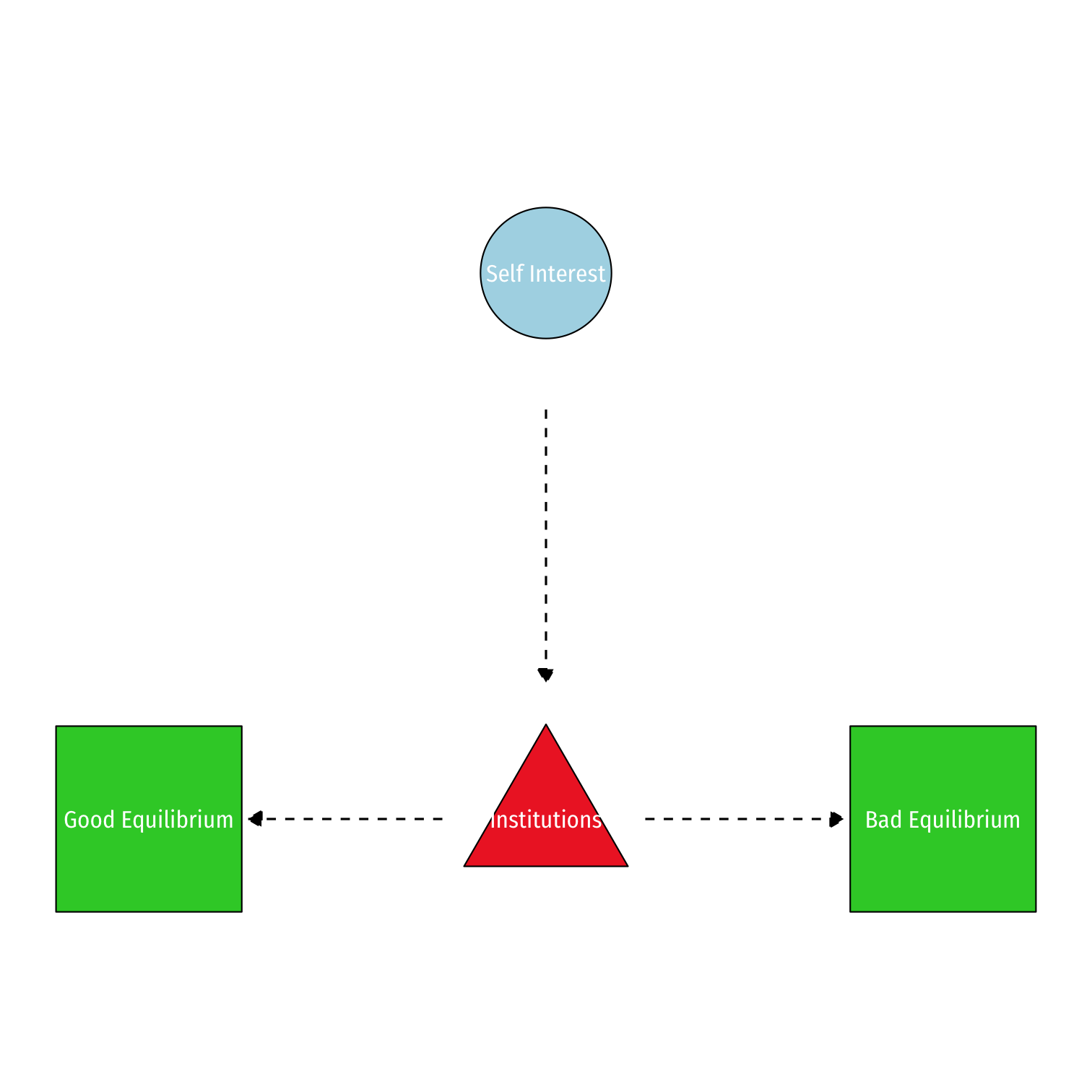

Institutions: Operationalizing Adam Smith

Adam Smith

1723-1790

“[Though] he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention...By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it,” (Book IV, Chapter 2.9).

Smith, Adam, 1776, An Enquiry into the Nature and Causes of the Wealth of Nations

Self-Interest Doesn’t Always Benefit Society

Institutions: Operationalizing Adam Smith

“[Though] he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention...By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it,” (Book IV, Chapter 2.9).

Smith, Adam, 1776, An Enquiry into the Nature and Causes of the Wealth of Nations

Institutions: Operationalizing Adam Smith

"[Though] he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention...By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it," (Book IV, Chapter 2.9).

Smith, Adam, 1776, An Enquiry into the Nature and Causes of the Wealth of Nations

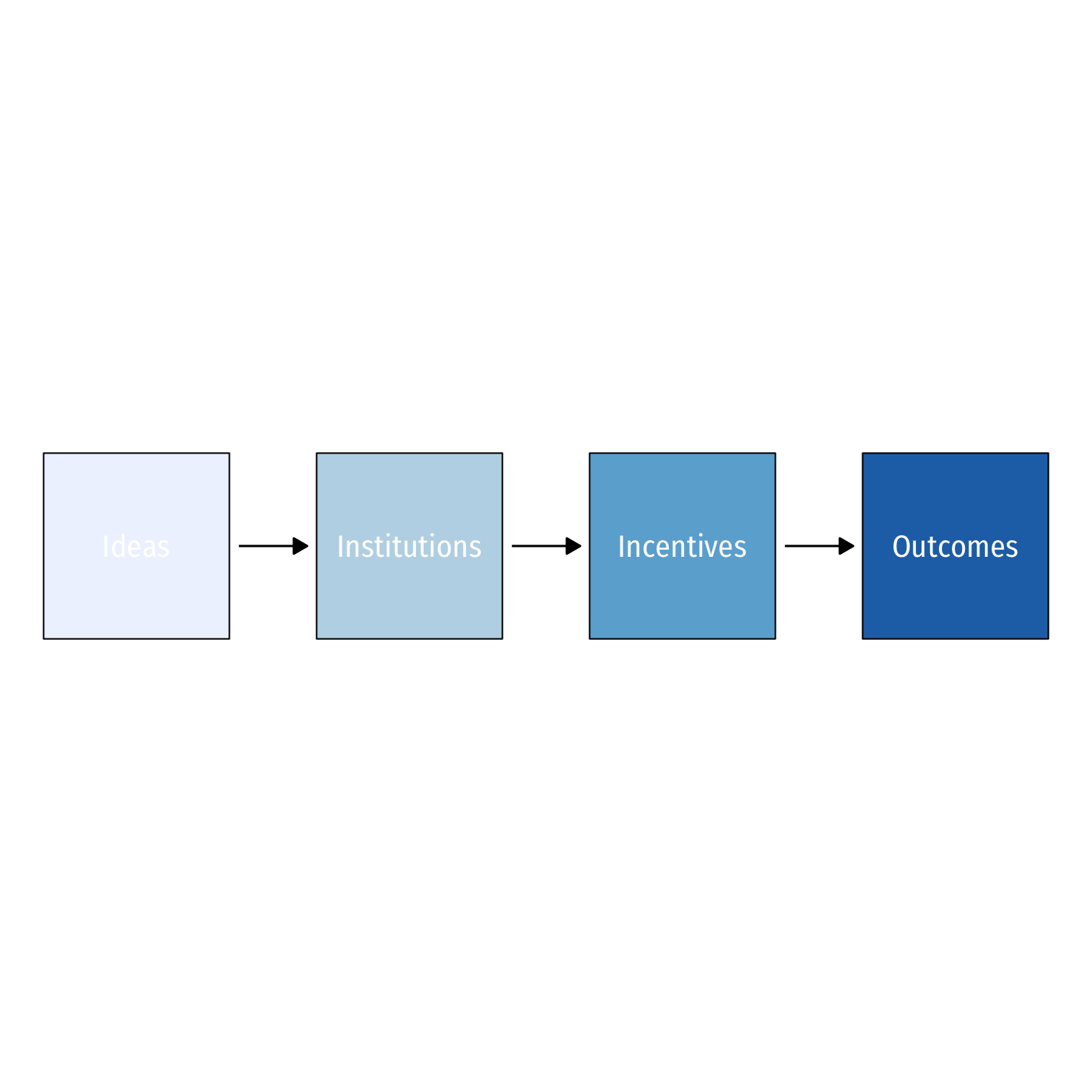

A Logical Framework for Political Economy

- Outcomes:

- relative level of wealth or poverty

- relative level of equality or inequality

- stability of politics, finance, macroeconomy

A Logical Framework for Political Economy

- Outcomes:

- relative level of wealth or poverty

- relative level of equality or inequality

- stability of politics, finance, macroeconomy

- ...are determined by Incentives:

- relative prices or costs of various choices

- profits and losses

- information

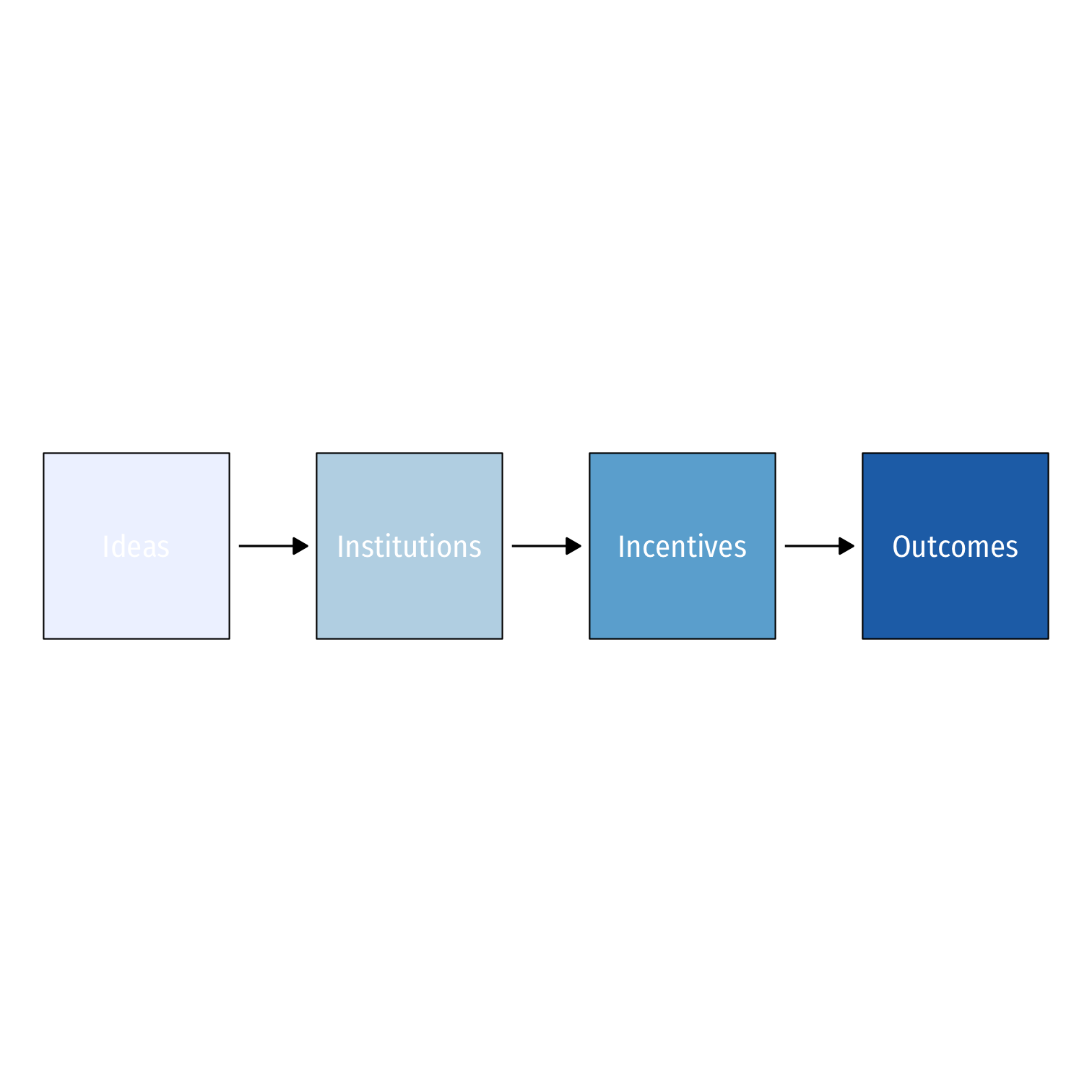

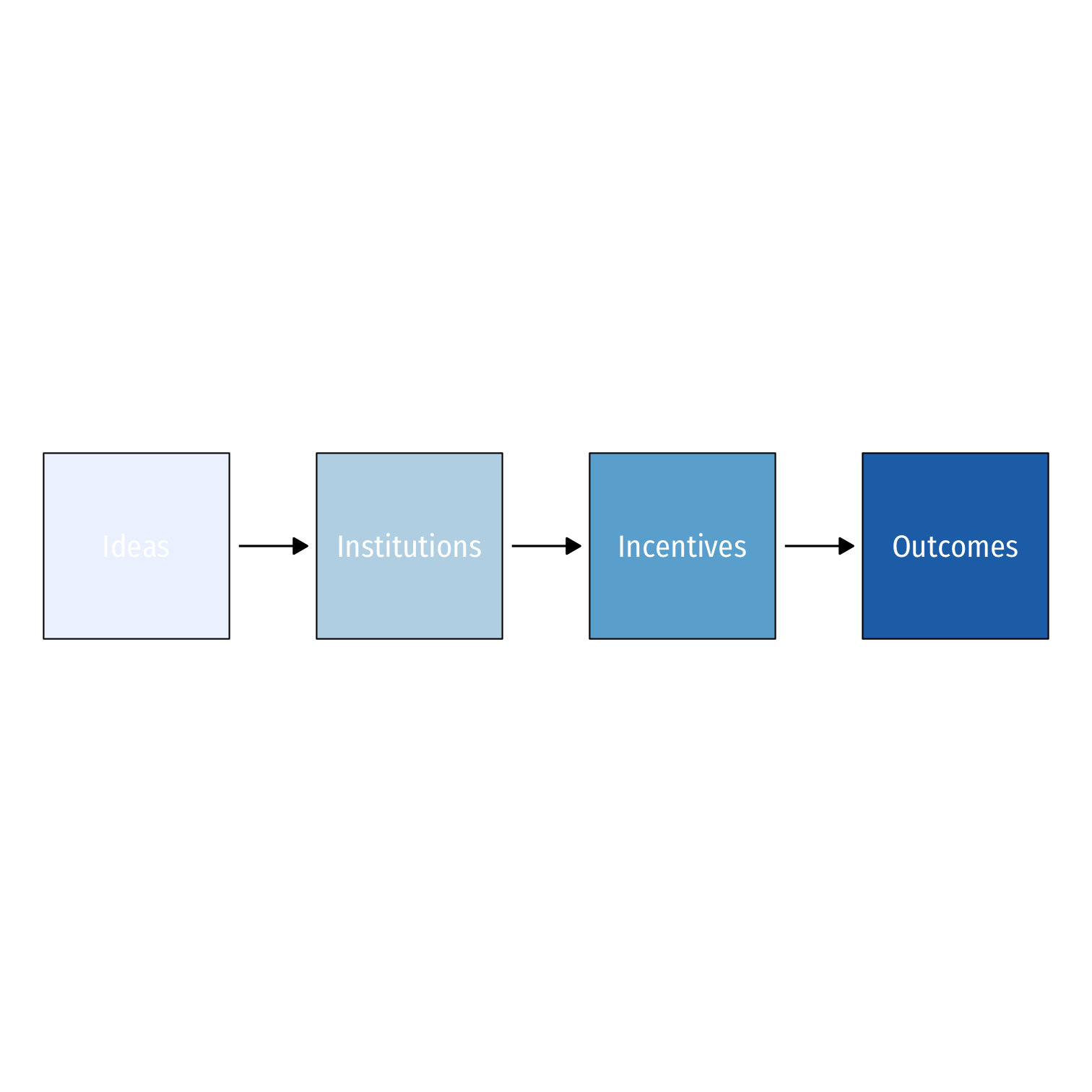

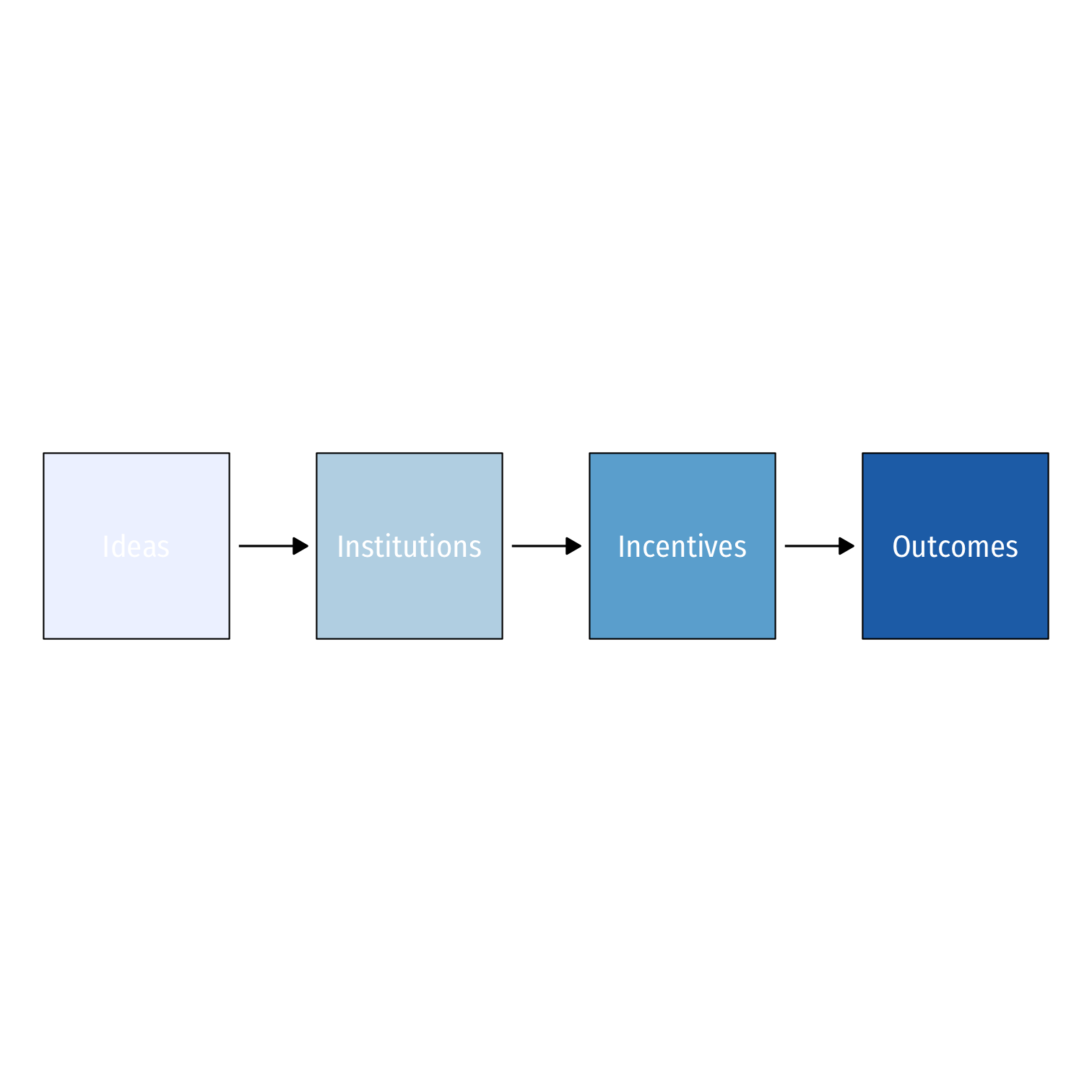

A Logical Framework for Political Economy

- Outcomes:

- relative level of wealth or poverty

- relative level of equality or inequality

- stability of politics, finance, macroeconomy

- ...are determined by Incentives:

- relative prices or costs of various choices

- profits and losses

- information

- ...are determined by Institutions:

- allocation of rights, property, & power

- (in)equality before the law or corruption

- constraints on politics and economics

A Logical Framework for Political Economy

- Outcomes:

- relative level of wealth or poverty

- relative level of equality or inequality

- stability of politics, finance, macroeconomy

- ...are determined by Incentives:

- relative prices or costs of various choices

- profits and losses

- information

- ...are determined by Institutions:

- allocation of rights, property, & power

- (in)equality before the law or corruption

- constraints on politics and economics

- ...are determined by Ideas:

- political and social worldview -"isms"

- which groups (should) have status

- moral and social norms

What are Institutions?

Douglass C. North

1920-2015

Economics Nobel 1993

“Institutions are the humanly devised constraints that structure political economic and social interaction. They consist of both informal constraints (sanctions, taboos, customs, traditions, and codes of conduct), and formal rules (constitutions, laws, property rights),” (p.10)

“Institutions are the rules of the game in a society,” (p.1).

North, Douglass C, (1991), "Institutions," Journal of Economic Perspectives 5(1): 97-112.

North, Douglass C, (1990), Institutions, Institutional Change, and Economic Performance

Incentives are Structured by Institutions

“Who needs this nail?”

“Don't worry about it! The main thing is that we immediately fulfilled the plan for nails!”

Institutions Channel Entrepreneurship

William Baumol

1922-2017

"If entrepreneurs are defined, simply, to be persons who are ingenious and creative in finding ways that add to their own wealth, power, and prestige, then it is to be expected that not all of them will be overly concerned with whether an activity that achieves these goals adds...to the social product," (pp.897-898).

"The rules of the game that determine the relative payoffs to different entrepreneurial activities do change dramatically from one time and place to another. Entrepreneurial behavior changes direction from one economy to another in a manner that corresponds to the variations in the rules of the game," (p.898).

Baumol, William J, (1990), "Entrepreneurship: Productive, Unproductive, and Destructive," Journal of Political Economy 98(5): 893-921

Profit Seeking and Rent Seeking

Productive entrepreneurship

Profits from serving customers

Unproductive entrepreneurship

Rents from political privileges

Destructive entrepreneurship

Loot from theft and violence