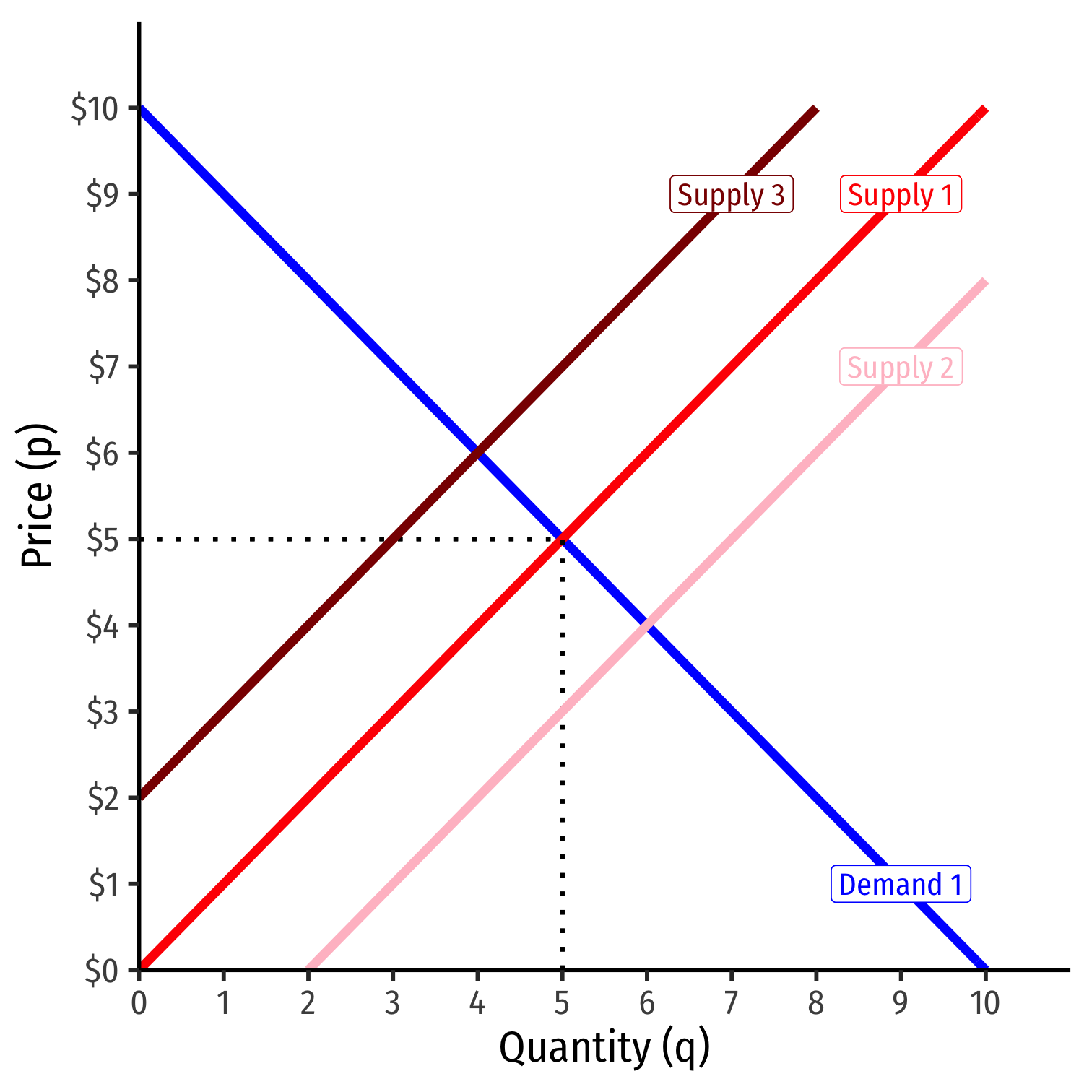

Entry/Exit Effects on Market Price

When all firms produce more/less; or firms enter or exit an industry, this affects the equilibrium market price

Think about basic supply & demand graphs:

- Entry: ↑ industry supply ⟹ ↑q,↓p

- Exit: ↓ industry supply ⟹ ↓q,↑p

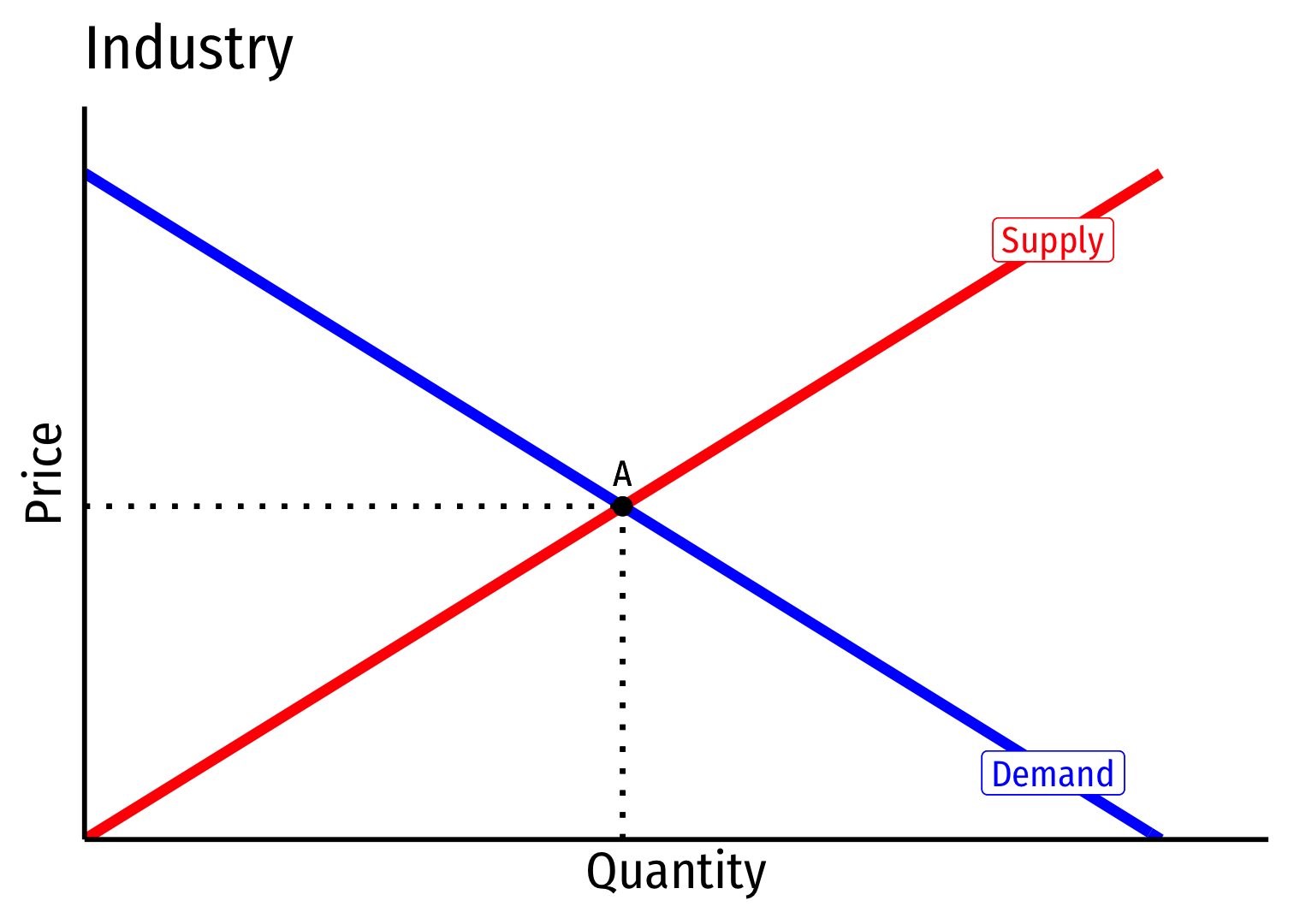

Constant Cost Industry (No External Economies) I

Constant cost industry has no external economies, no change in costs as industry output increases (firms enter & incumbents produce more)

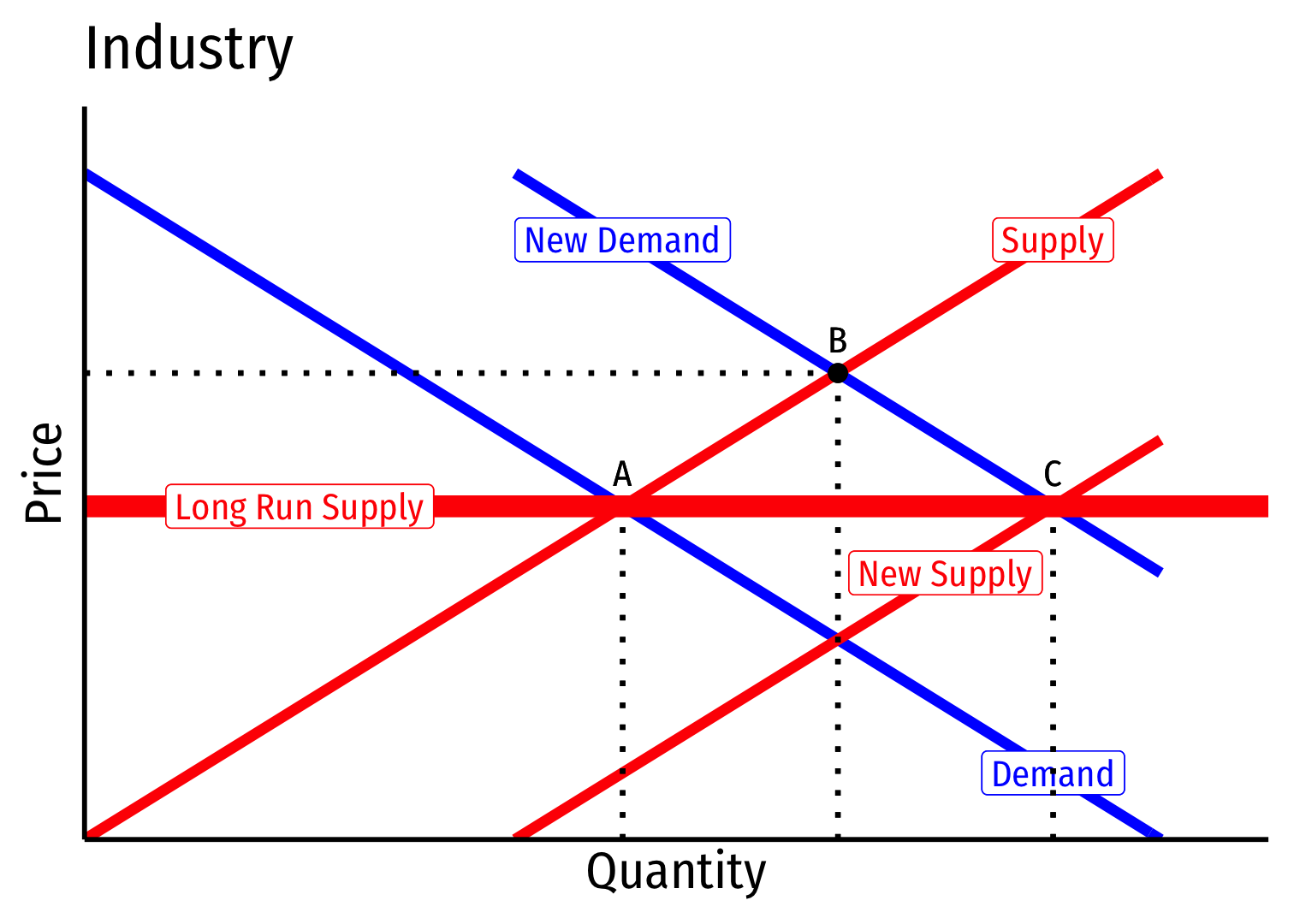

A perfectly elastic long-run industry supply curve!

Determinants:

- Industry's purchases are not a large share of input markets

- Often constant marginal costs, insignificant fixed costs

Examples: toothpicks, domain name registration, waitstaff

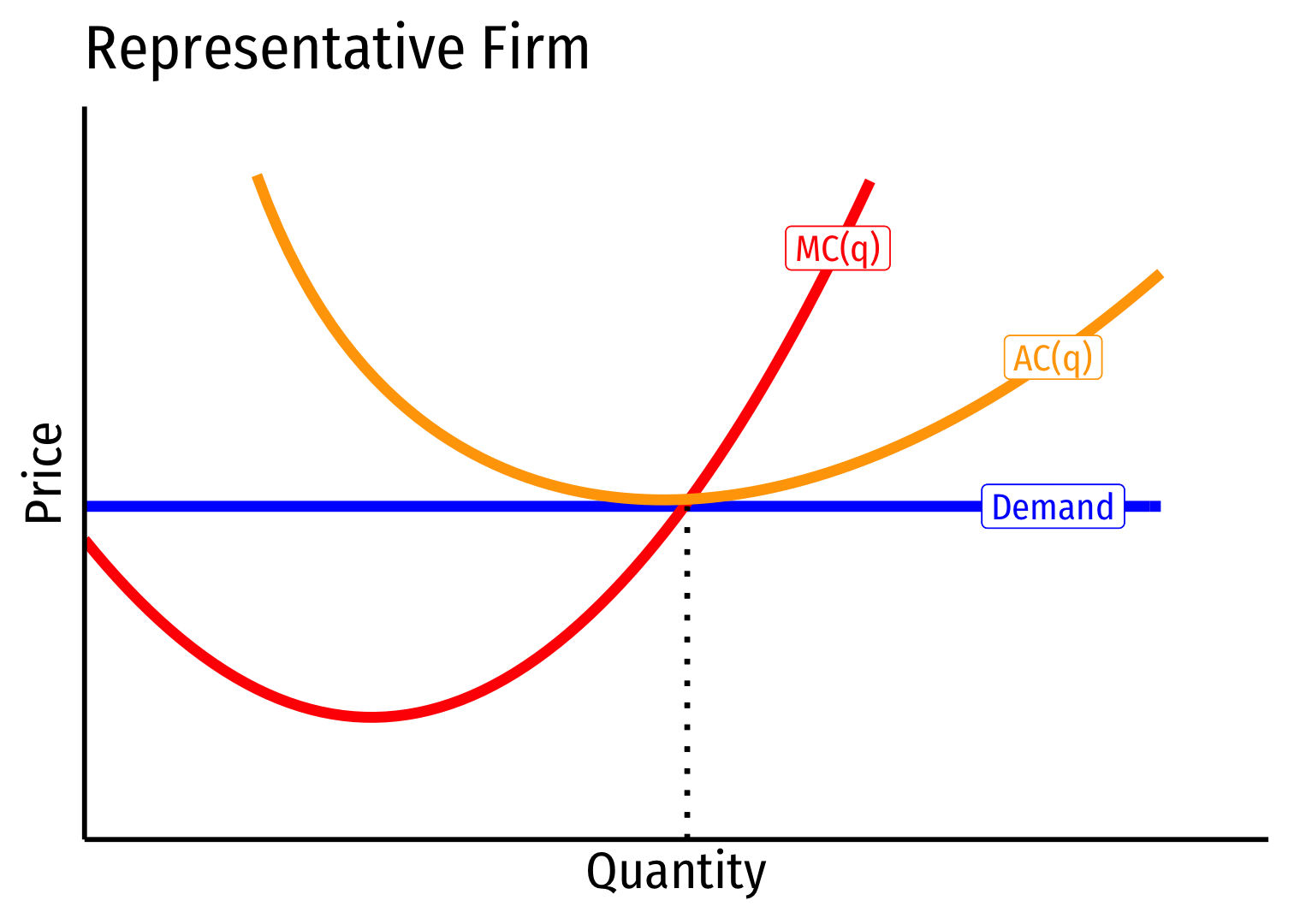

Constant Cost Industry (No External Economies) II

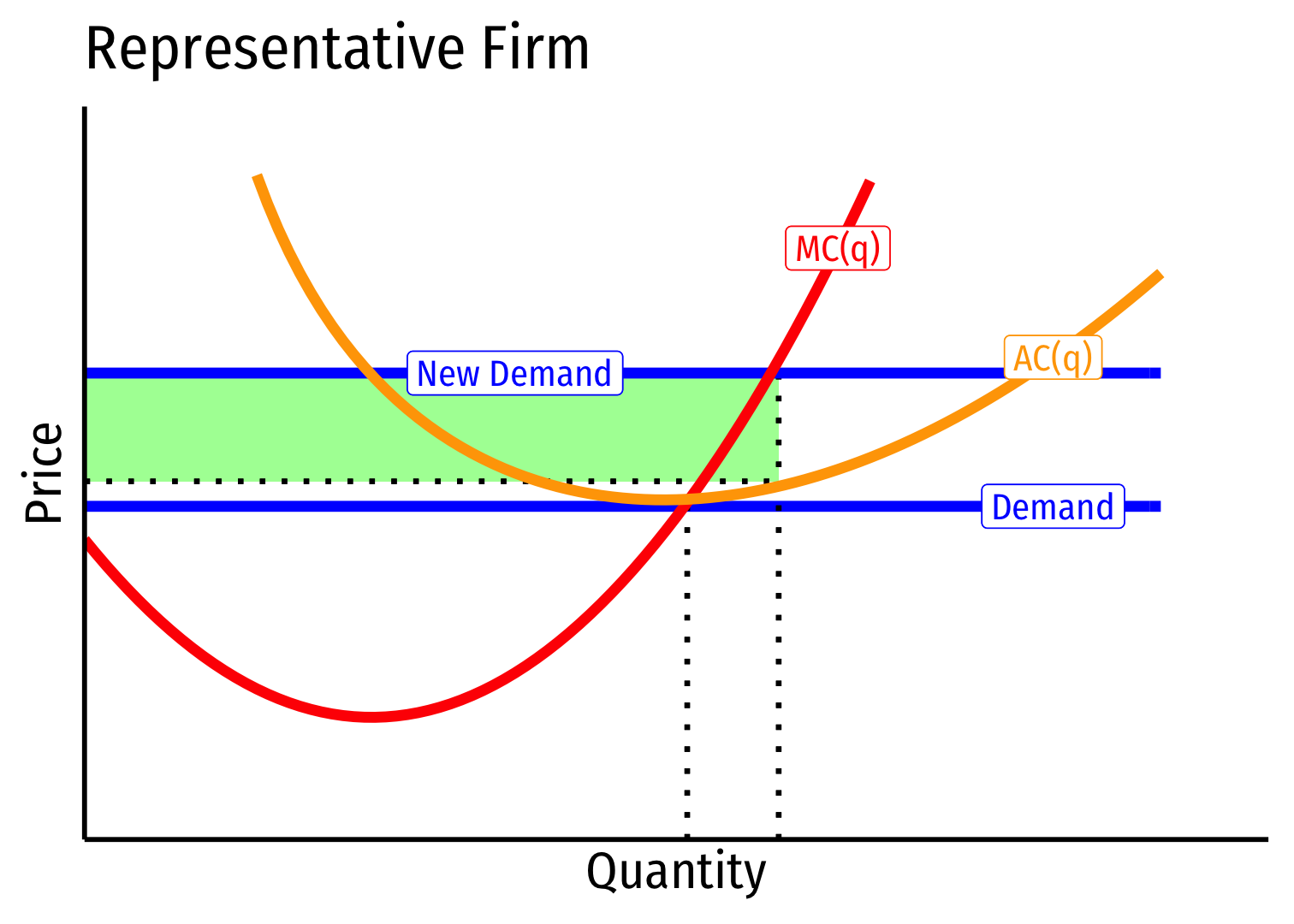

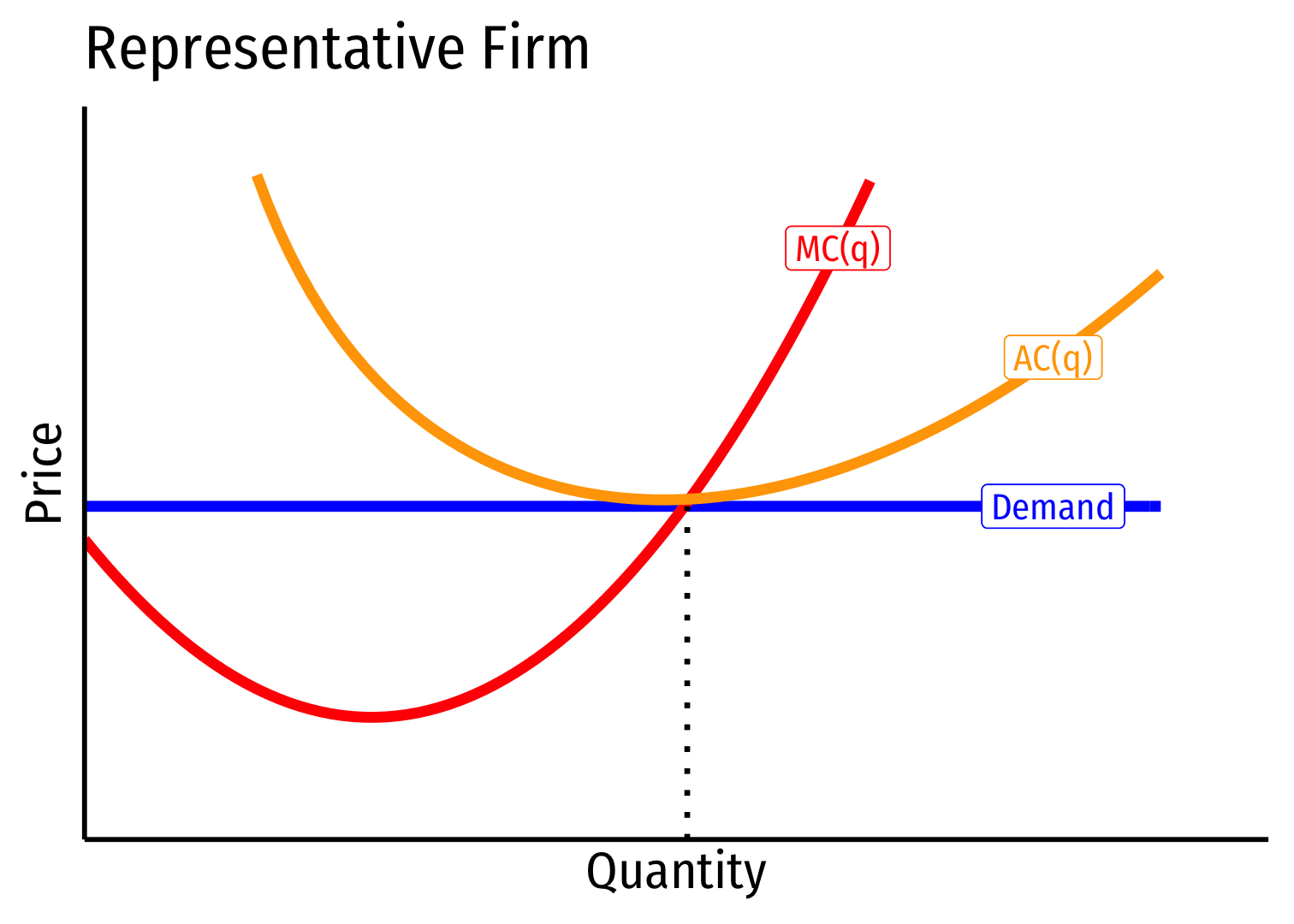

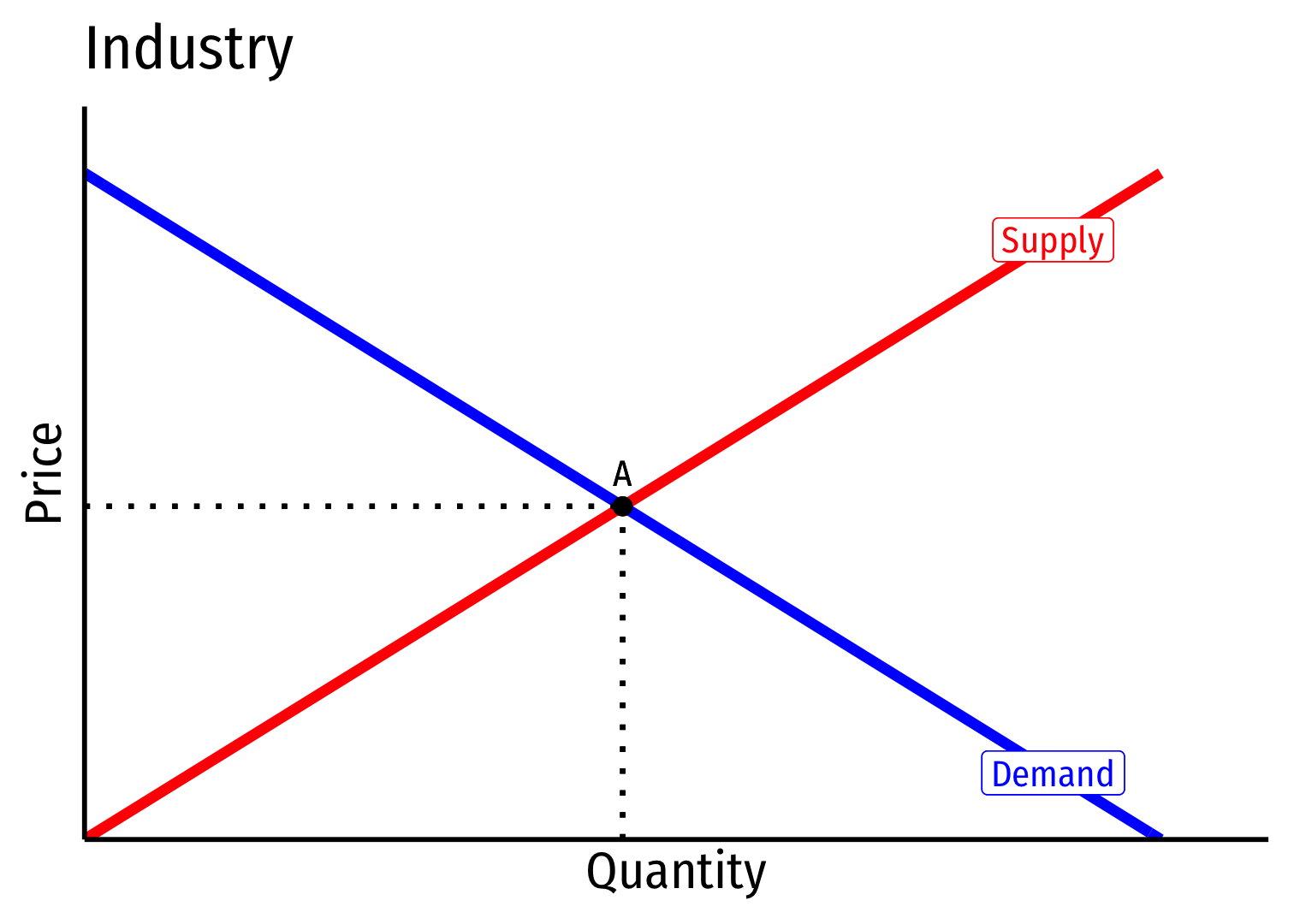

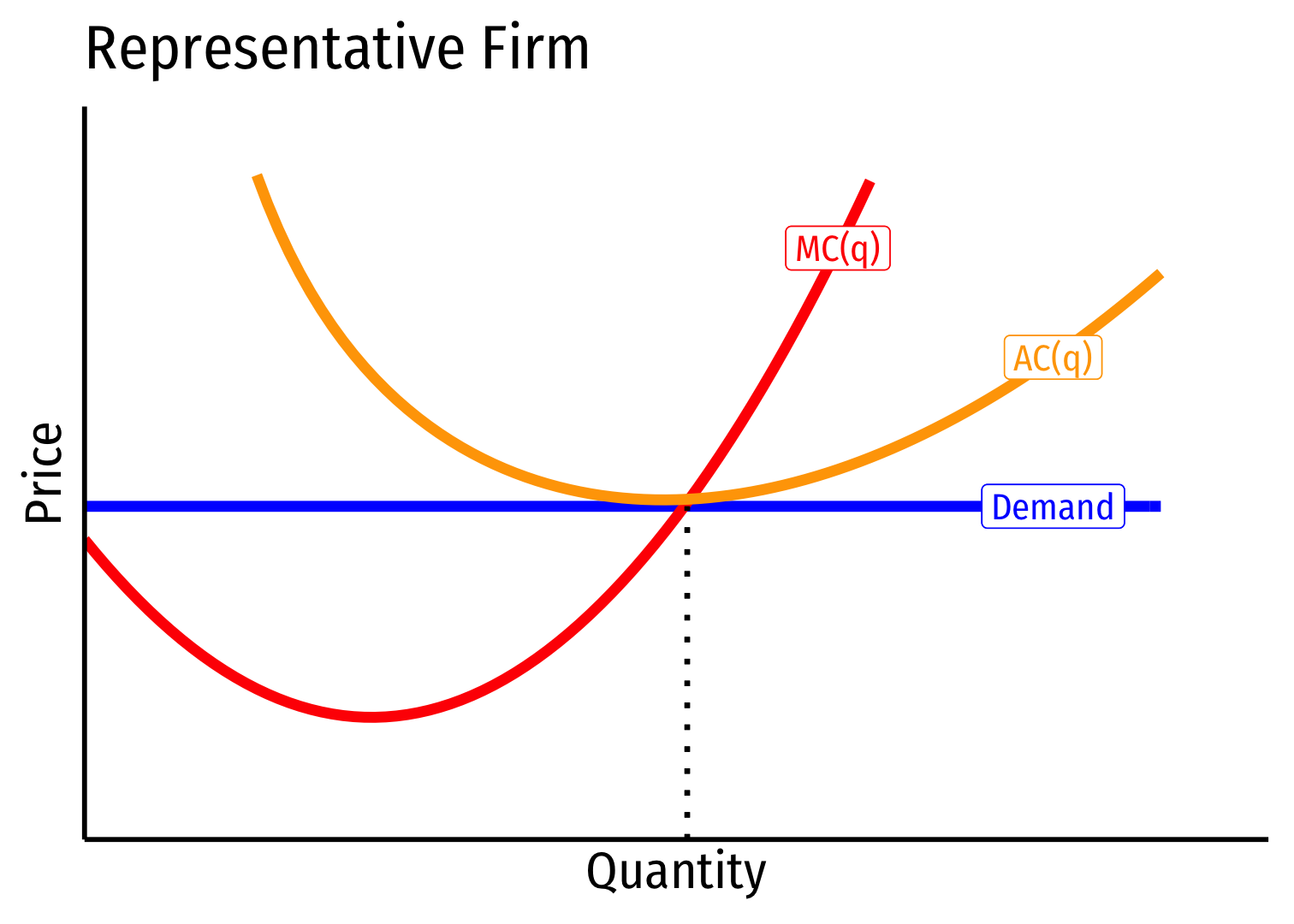

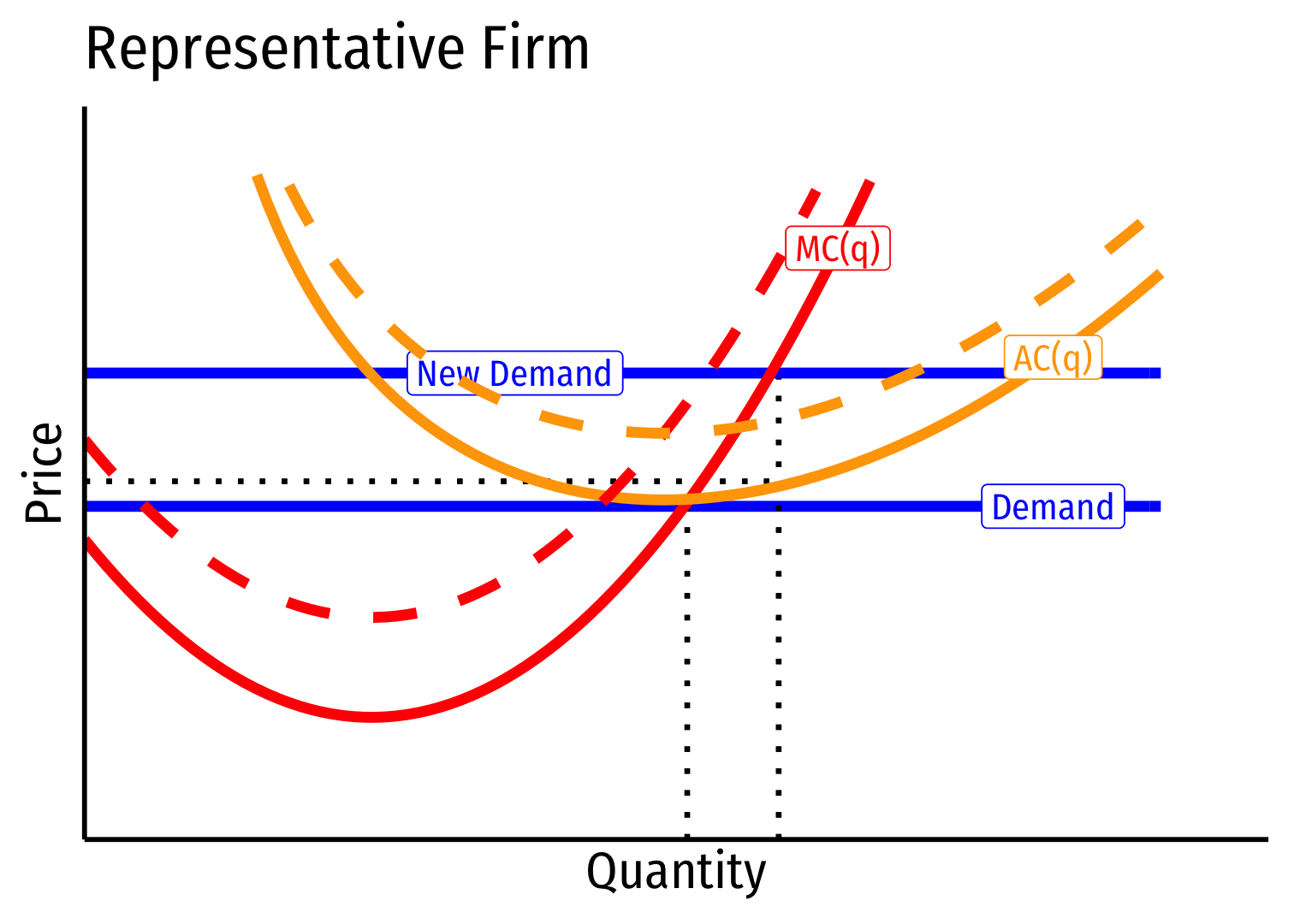

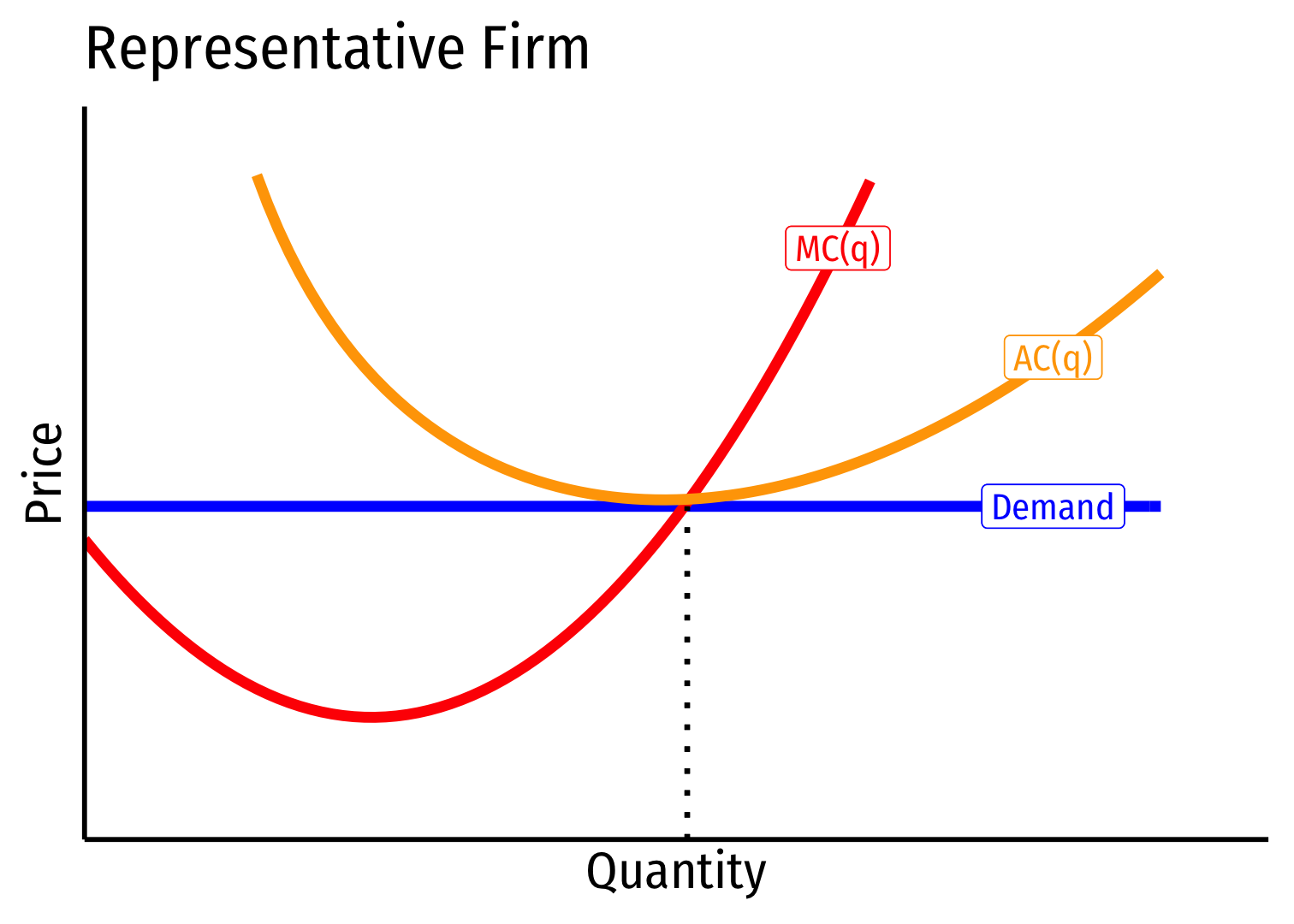

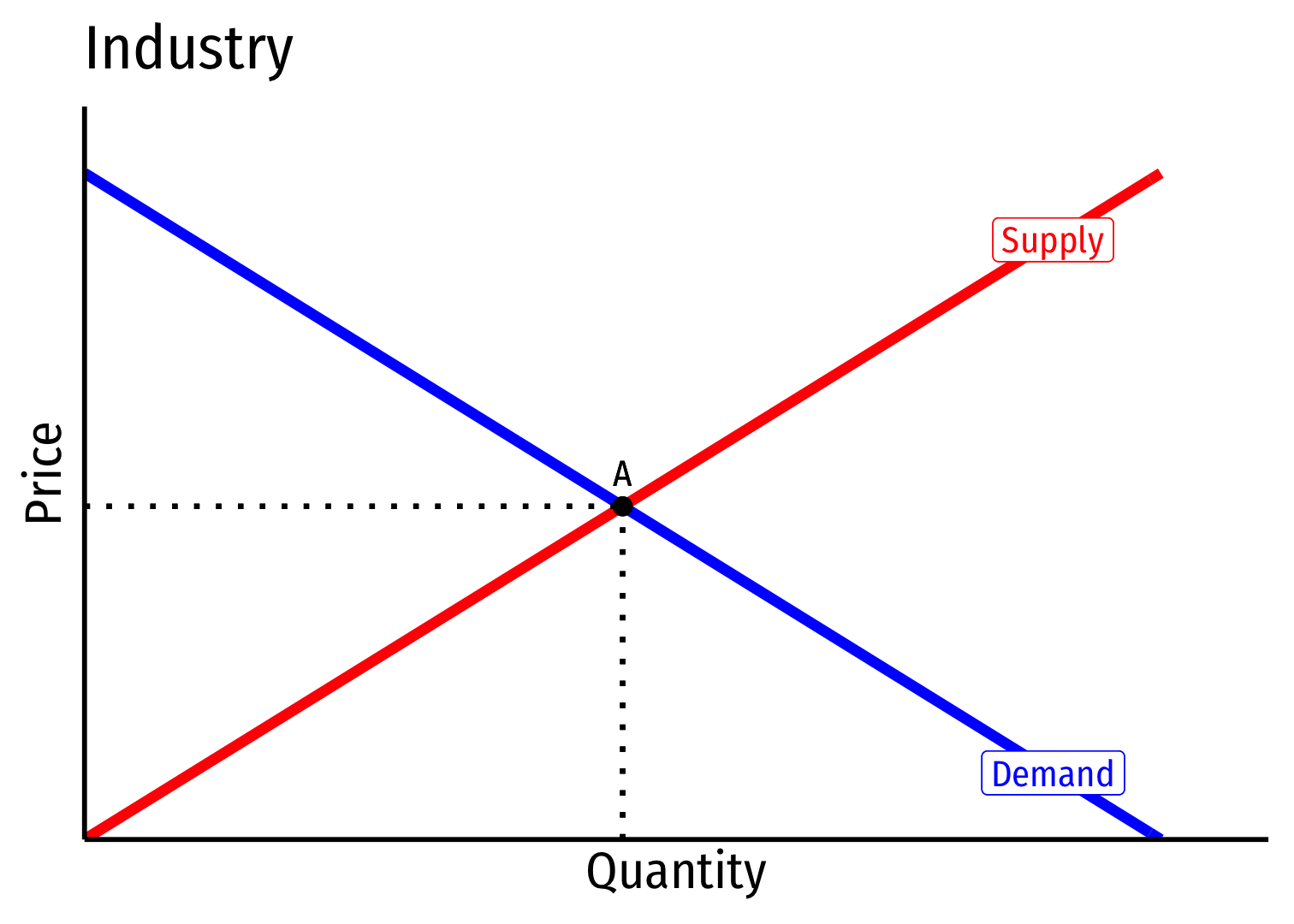

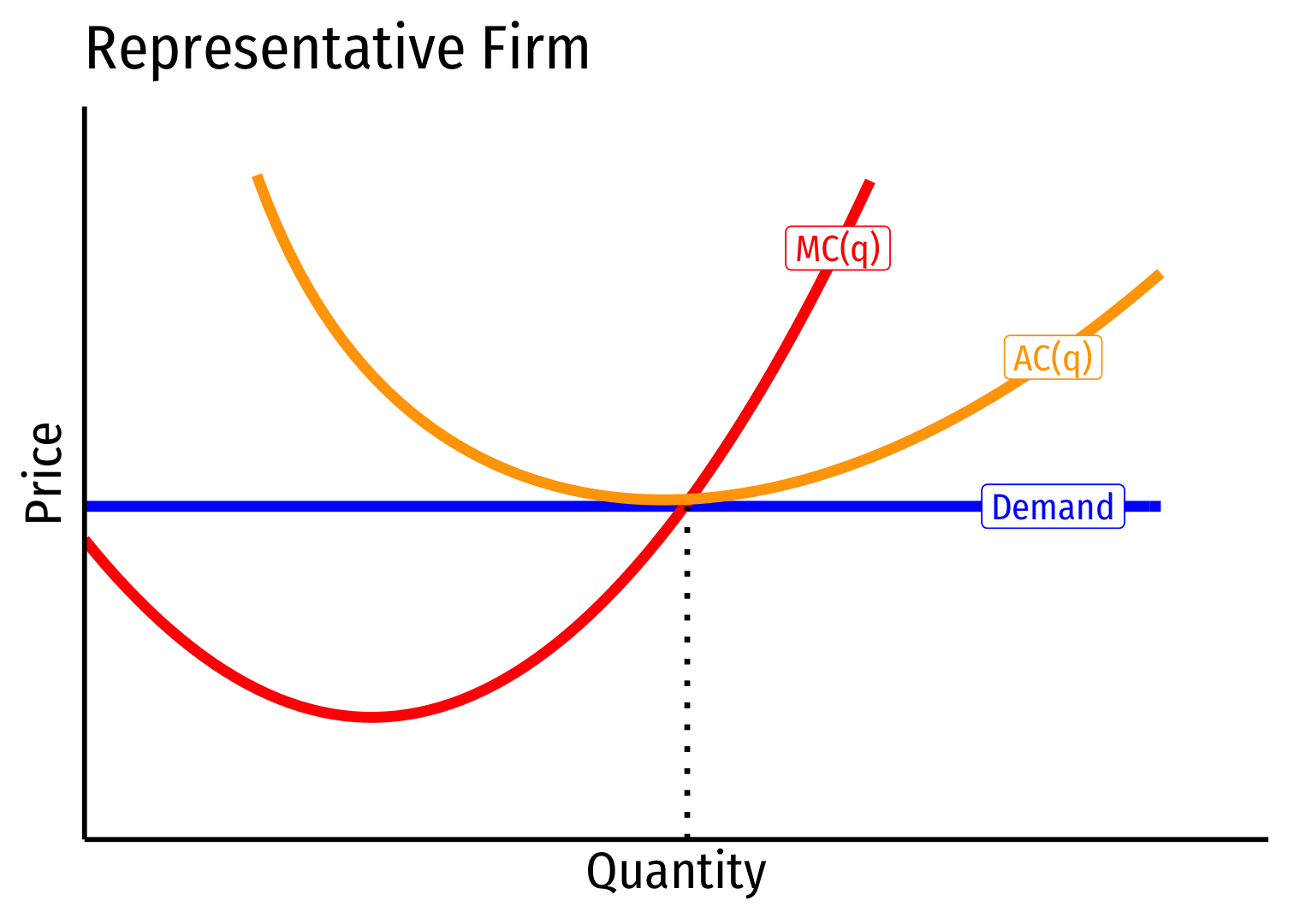

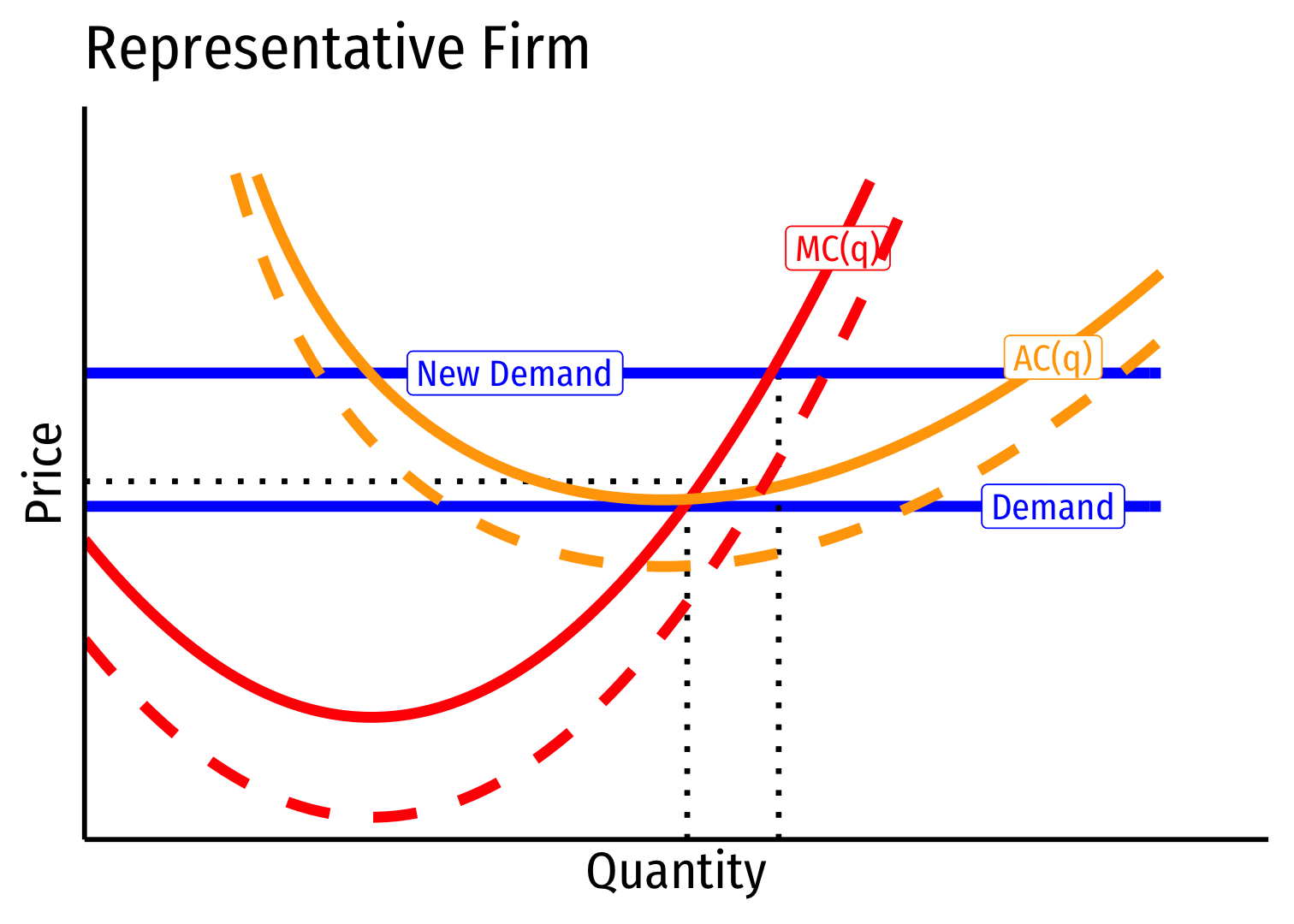

- Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

Constant Cost Industry (No External Economies) III

Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

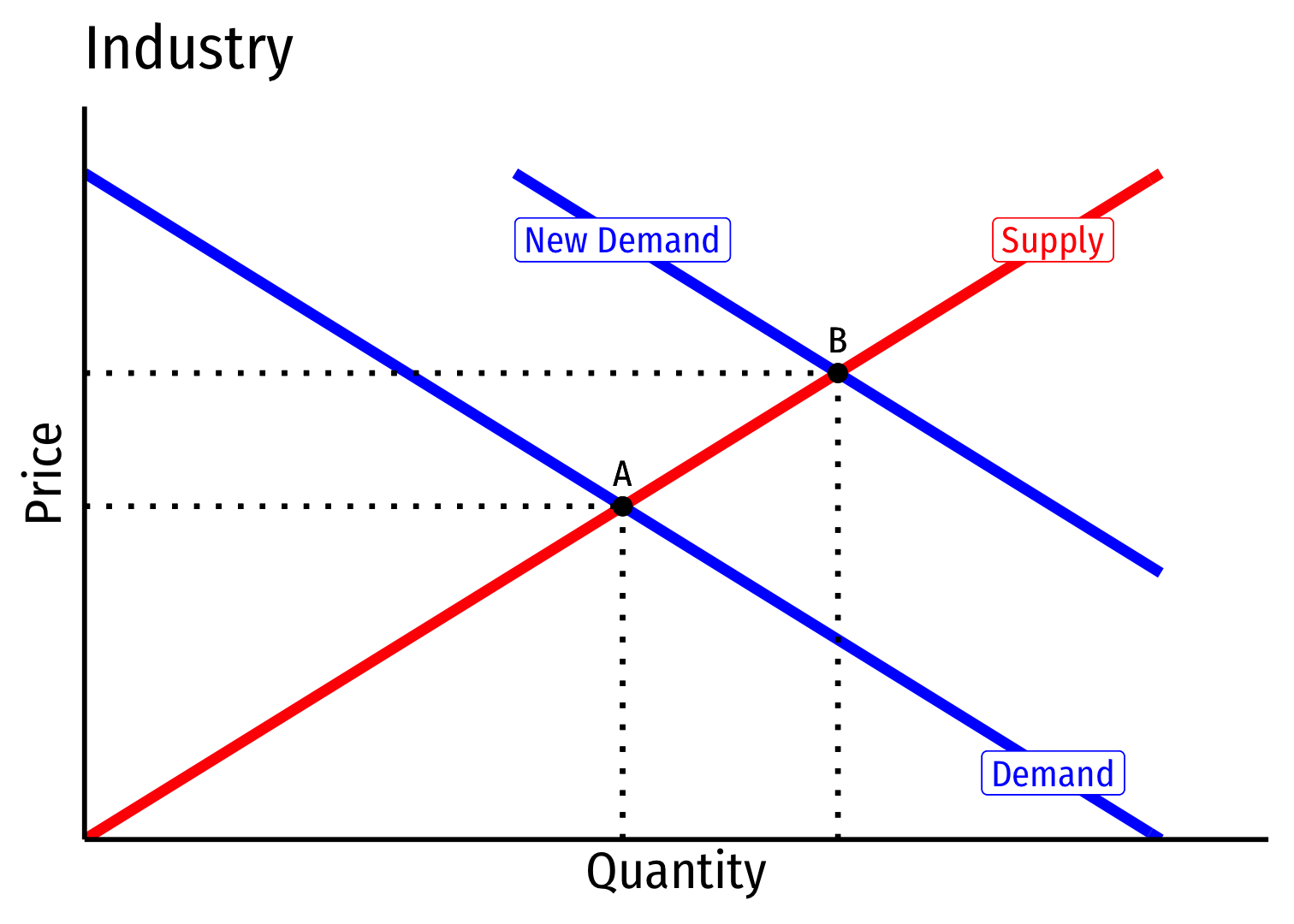

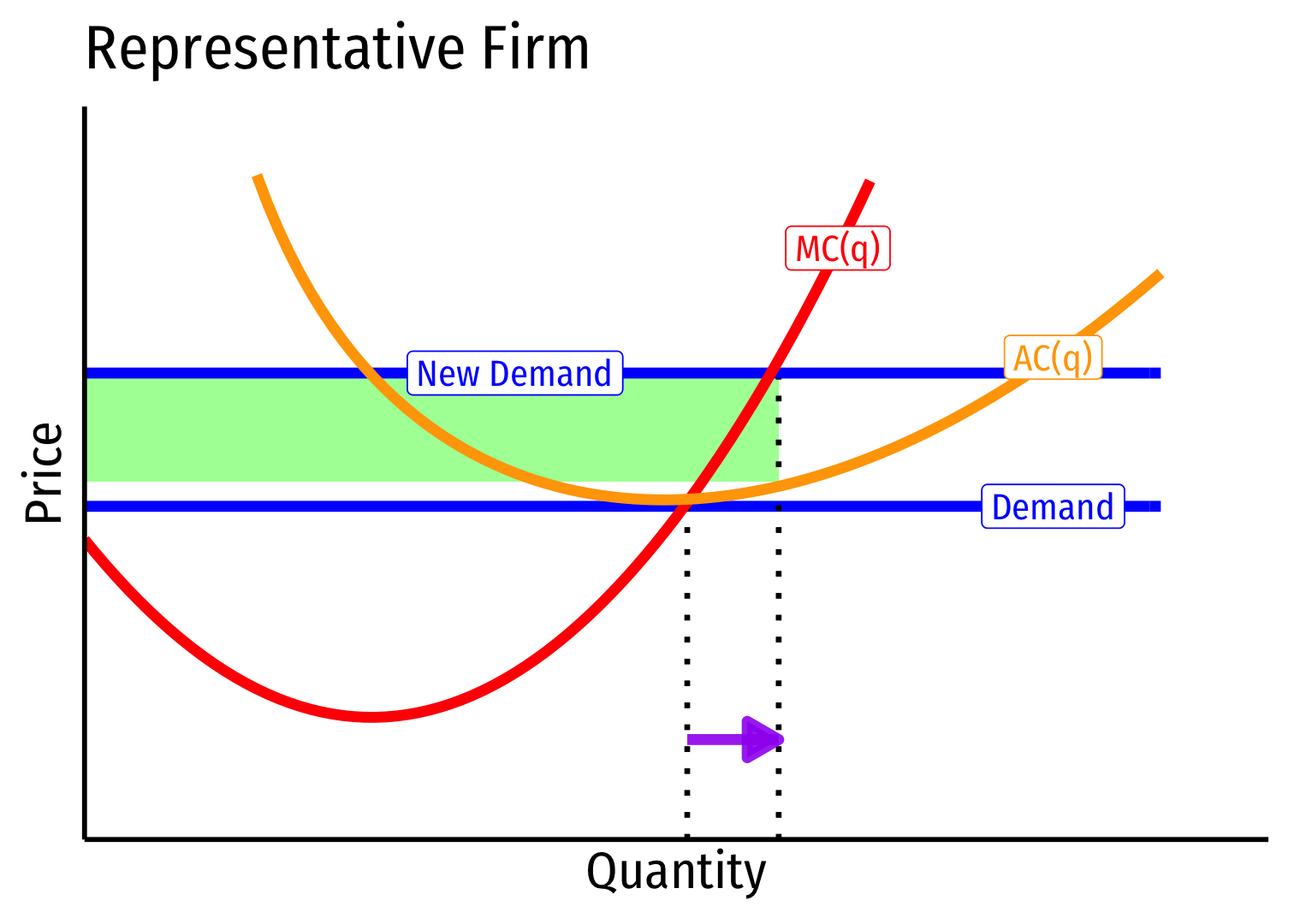

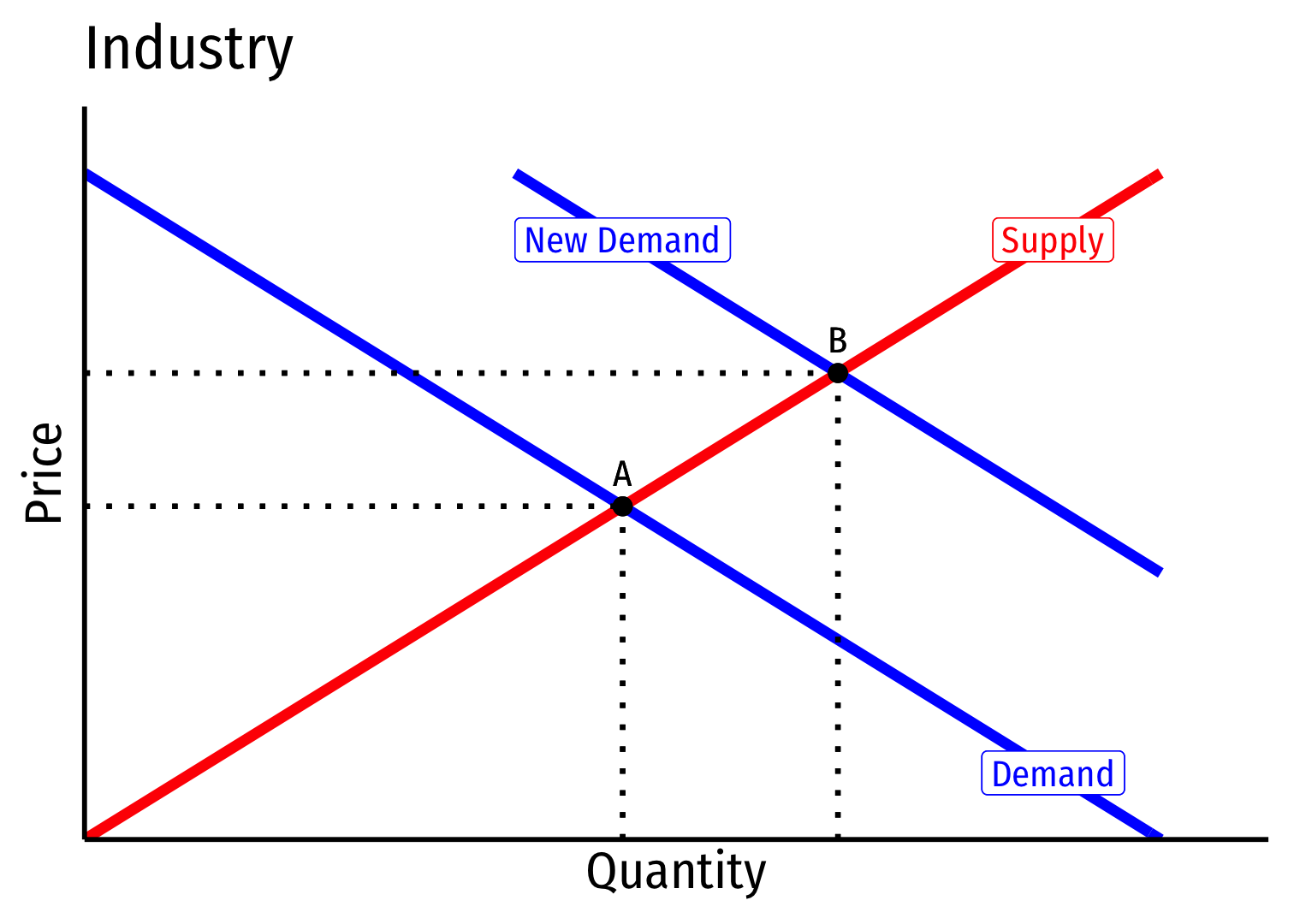

Exogenous increase in market demand

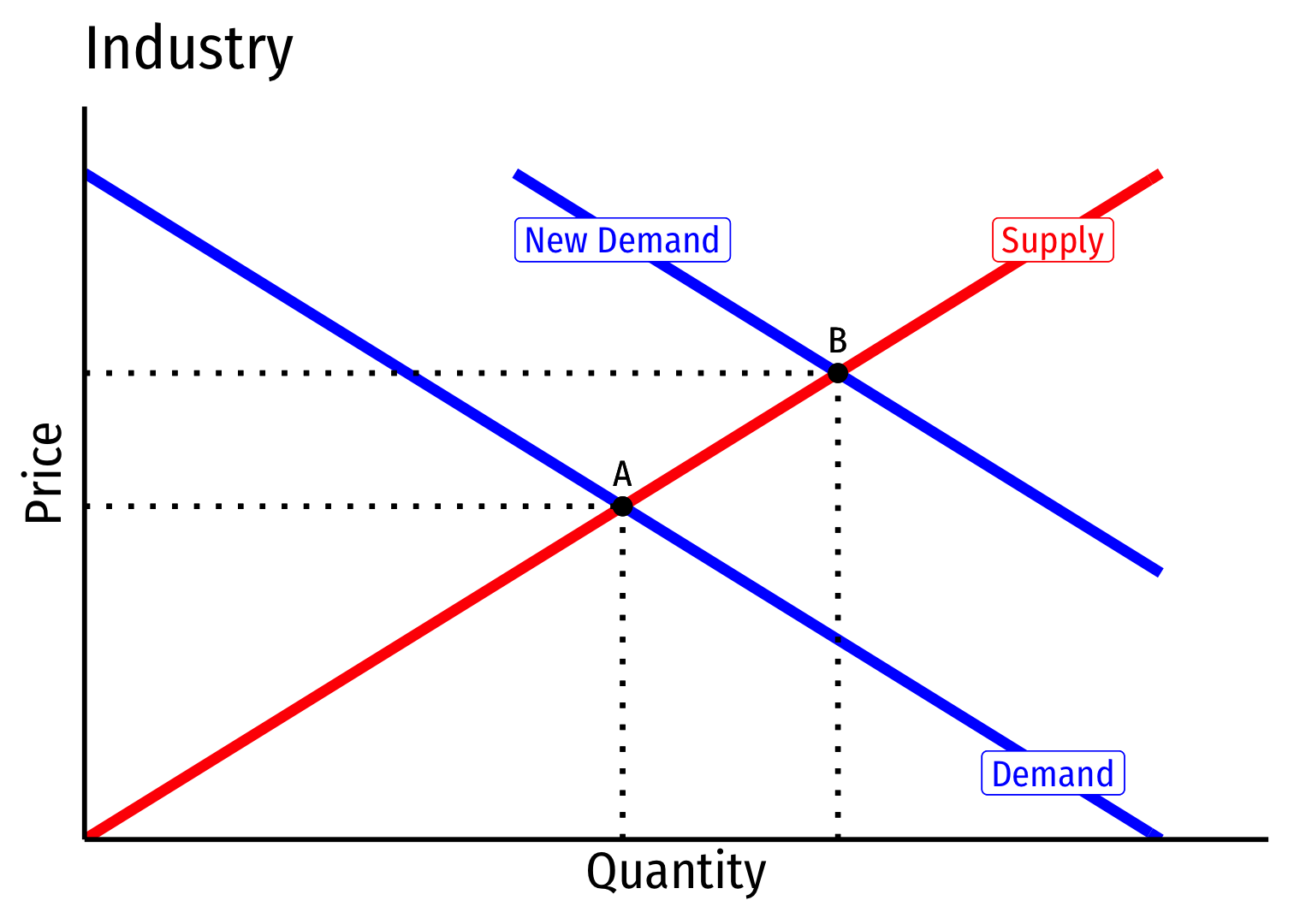

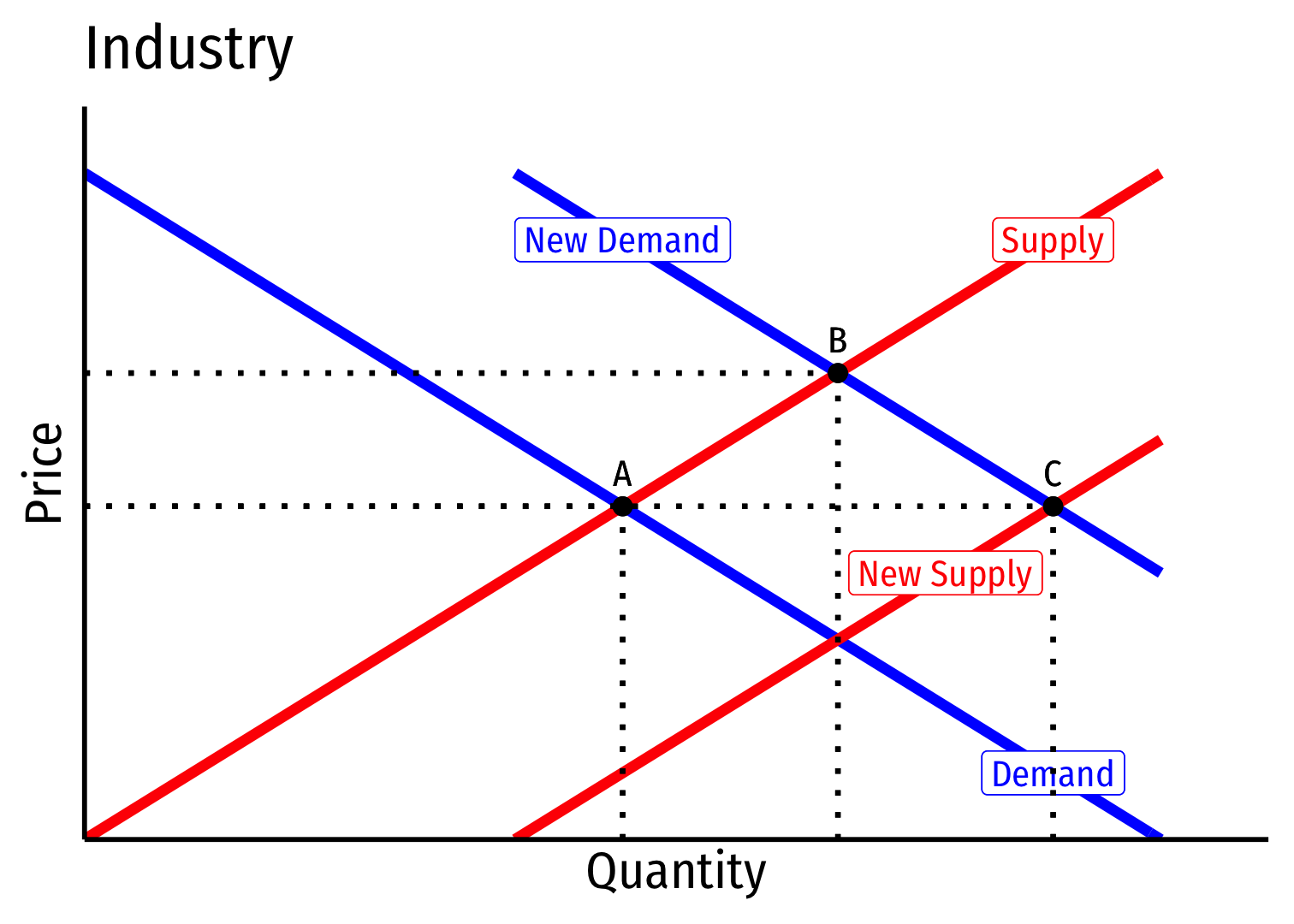

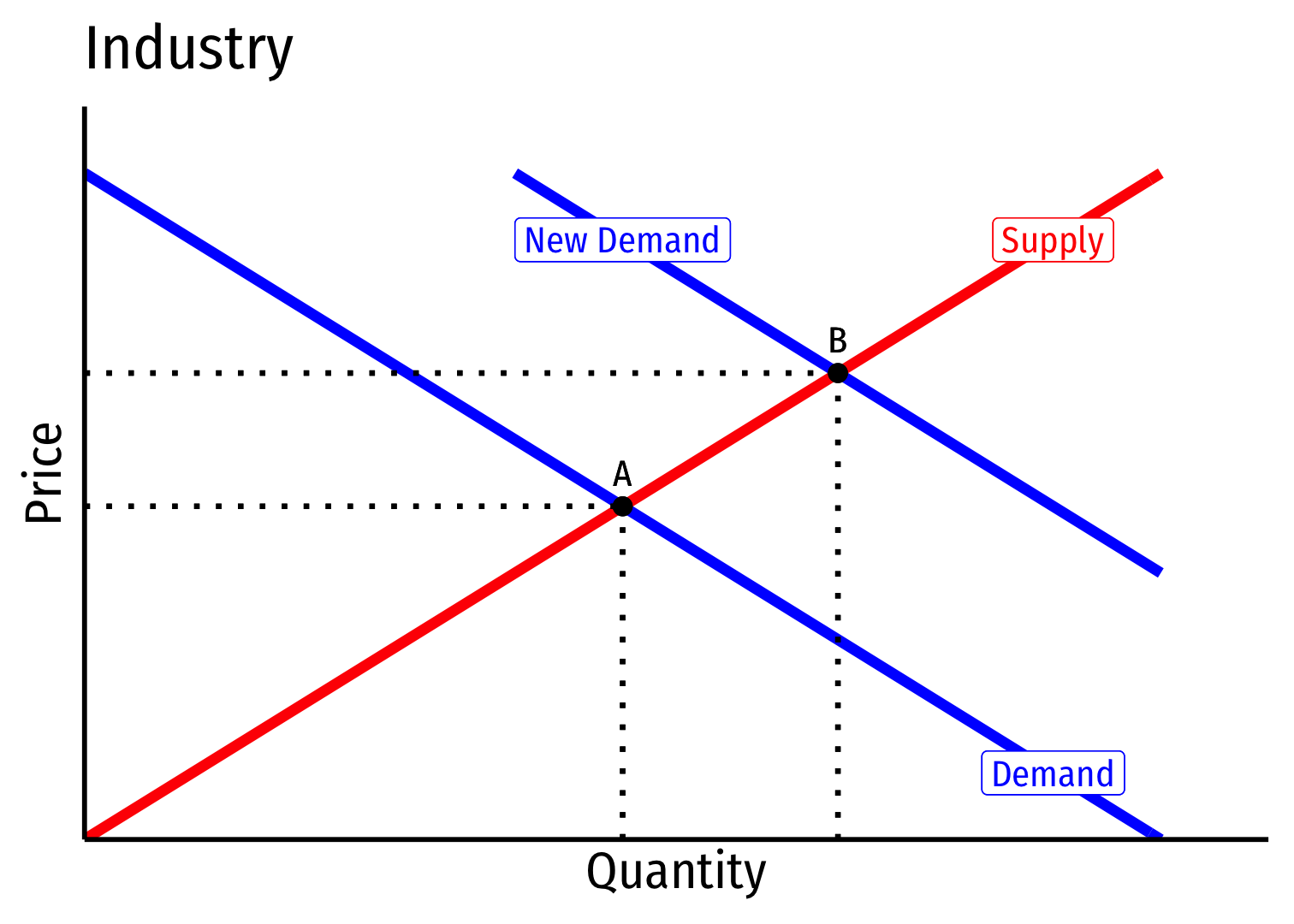

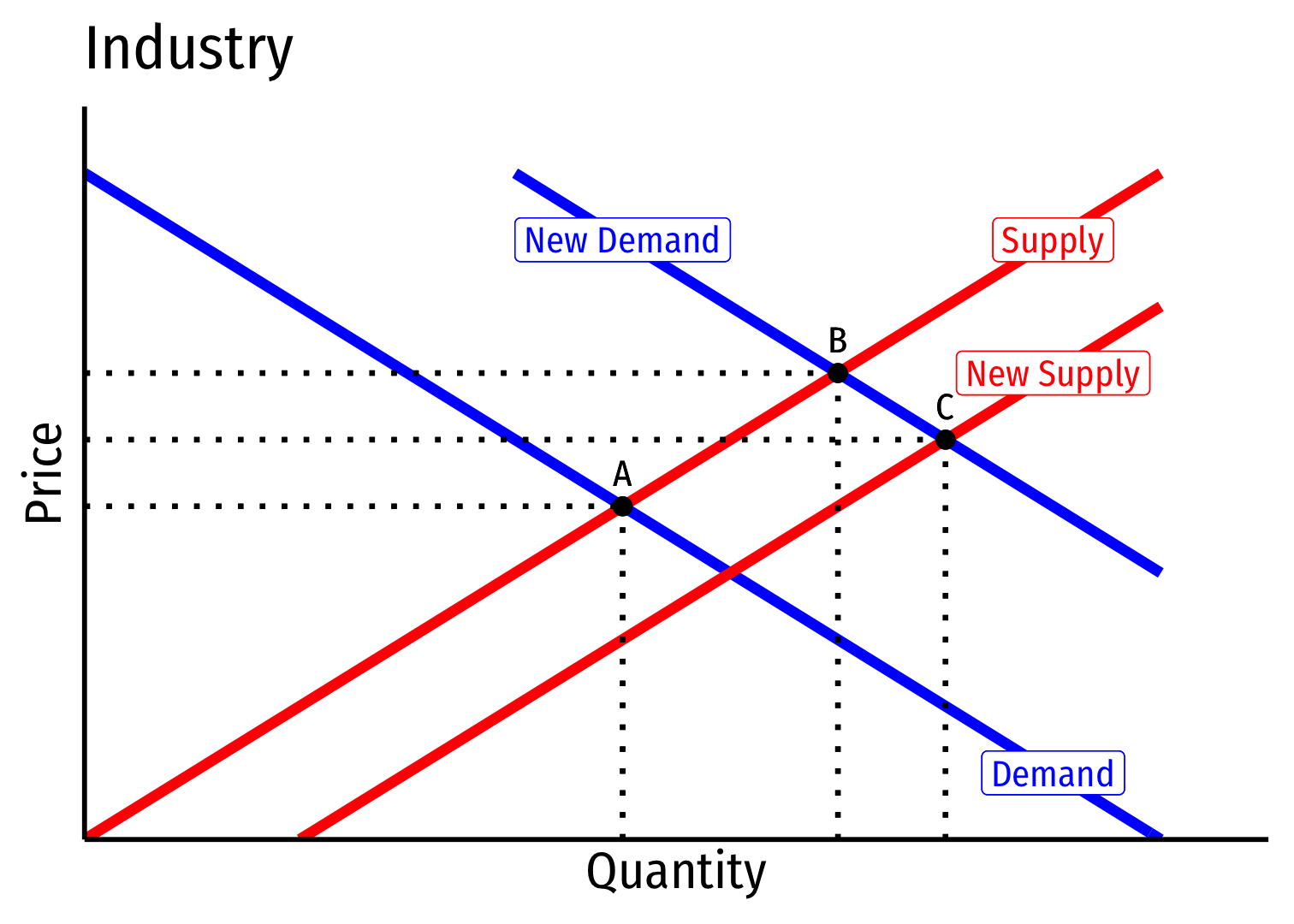

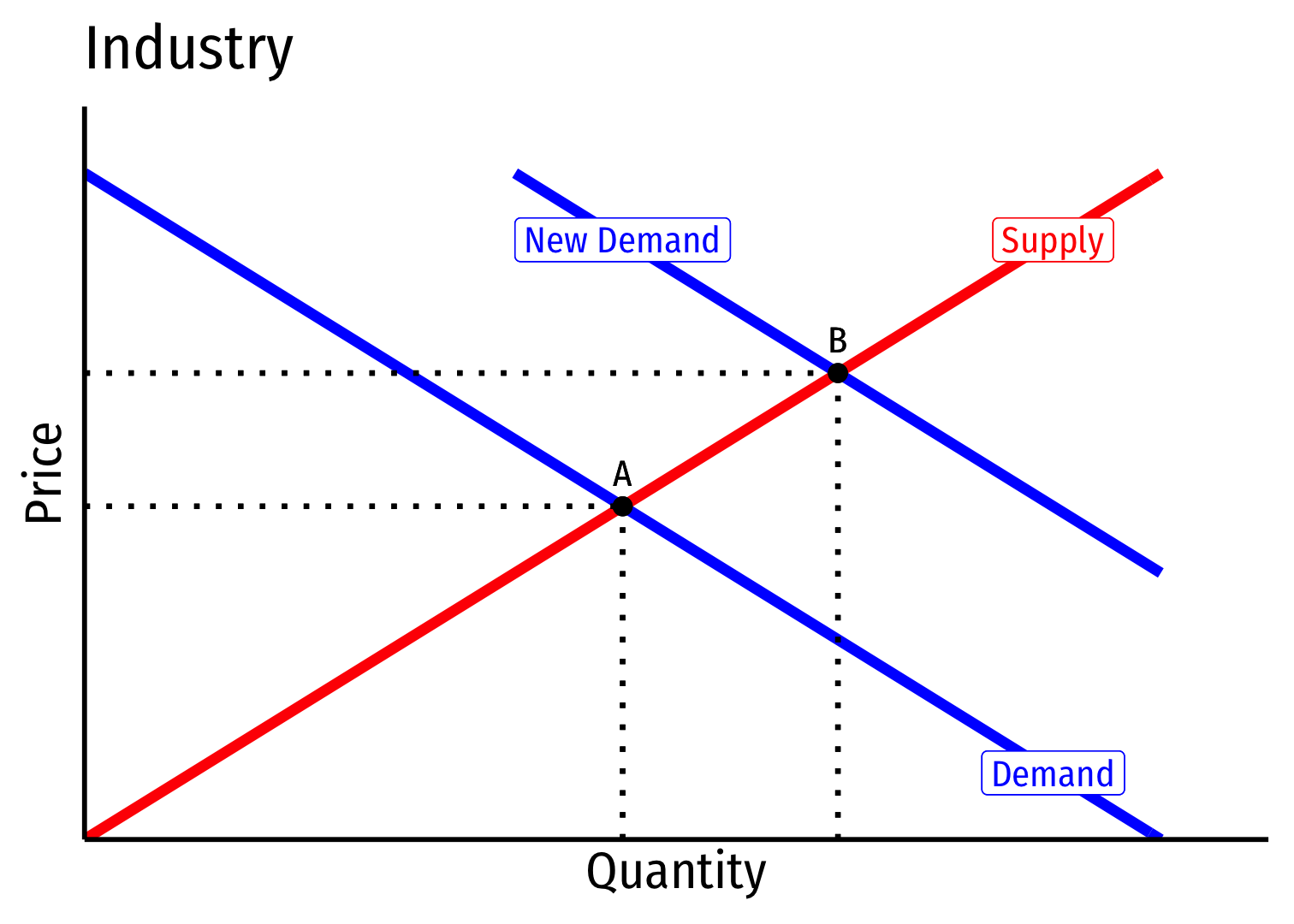

Constant Cost Industry (No External Economies) IV

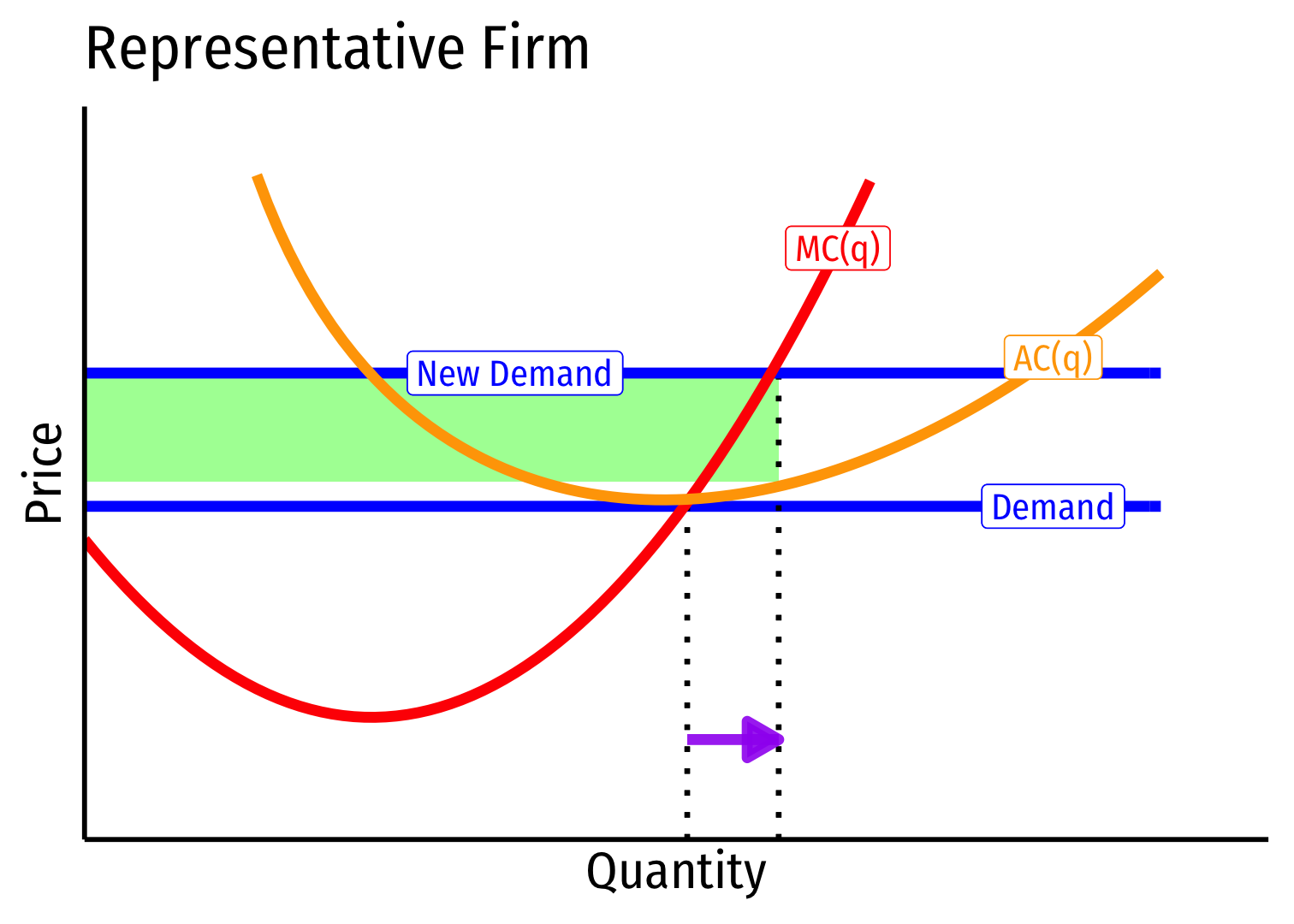

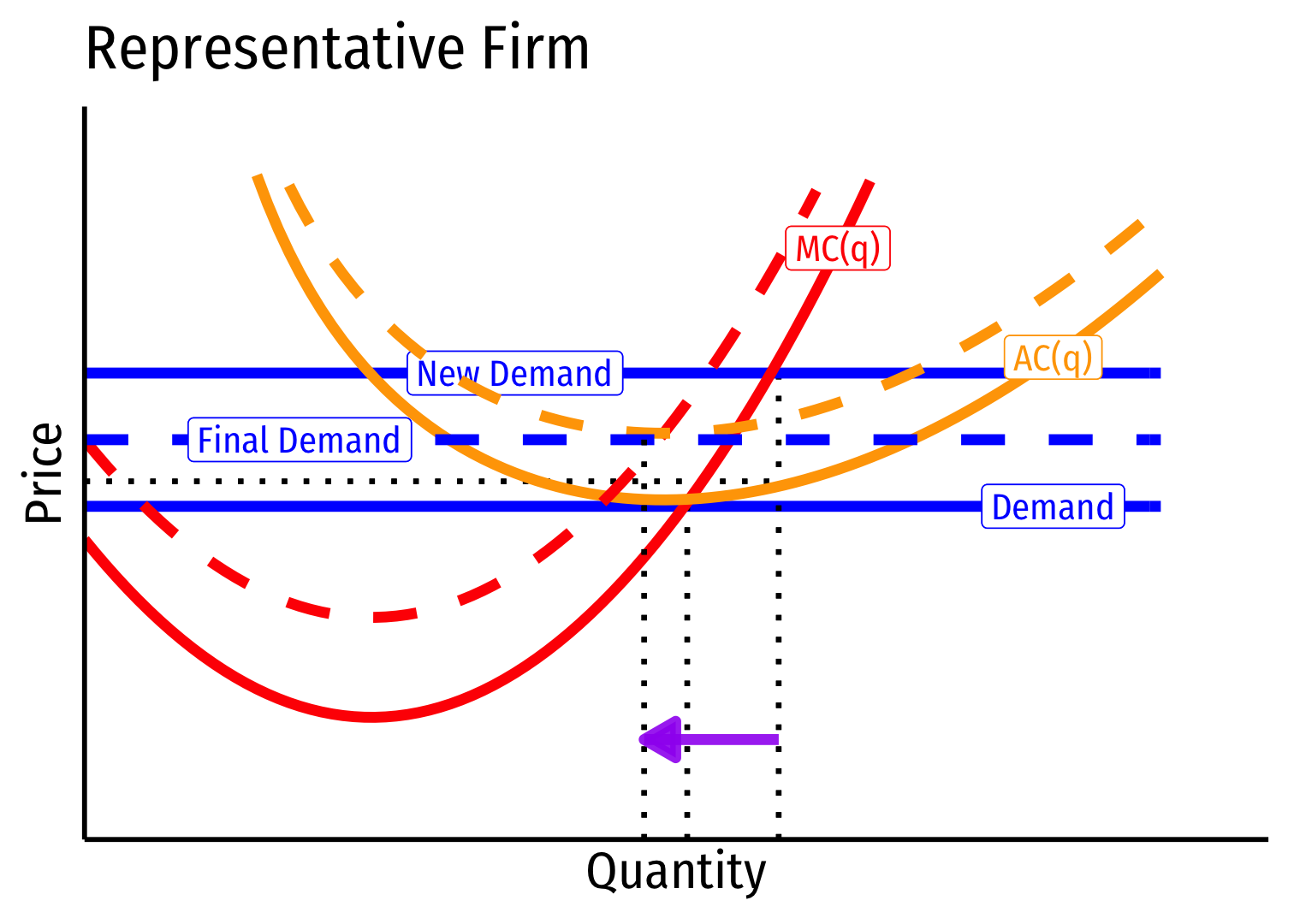

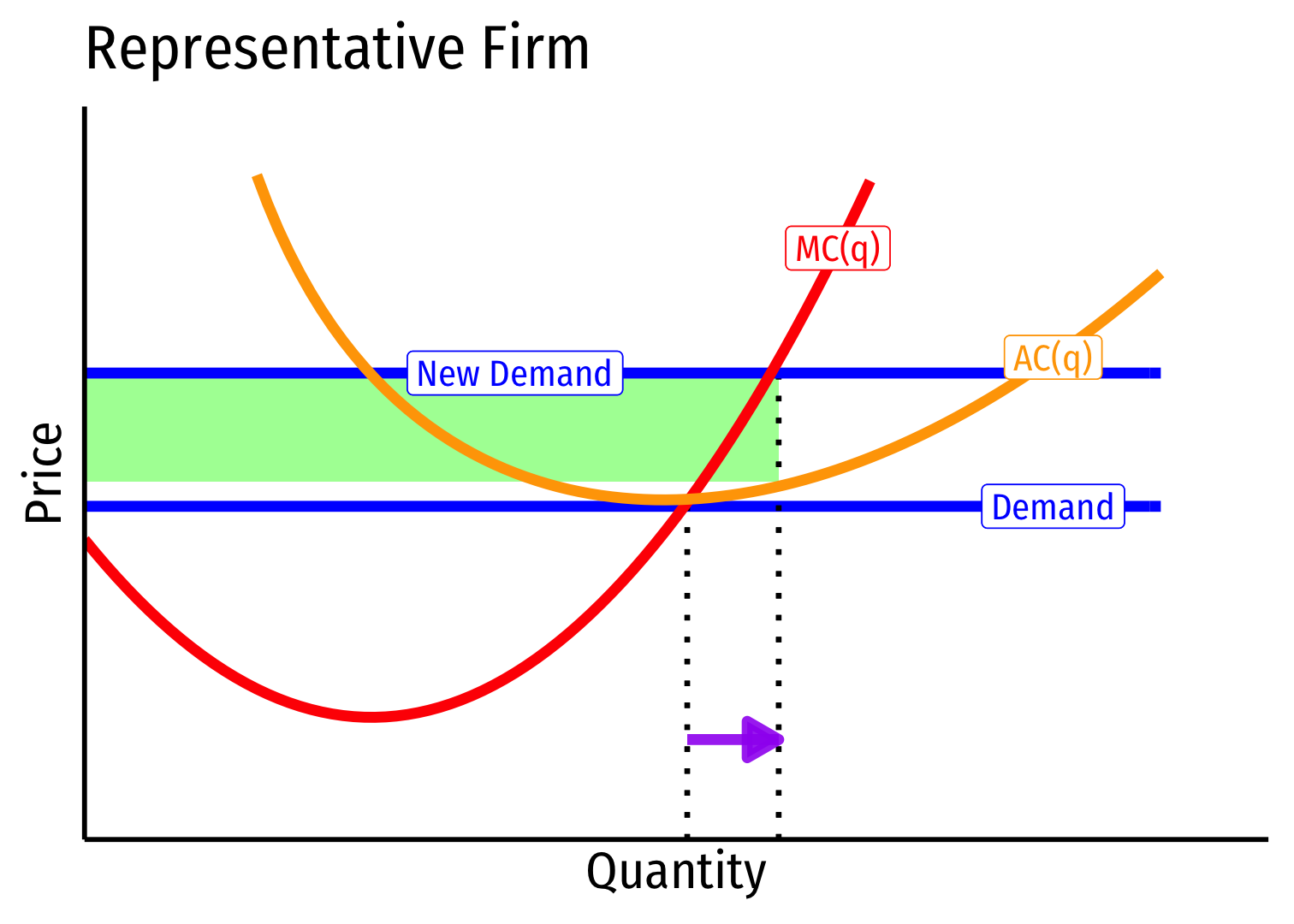

Short run (A→B): industry reaches new equilibrium

Firms charge higher p∗, produce more q∗, earn π

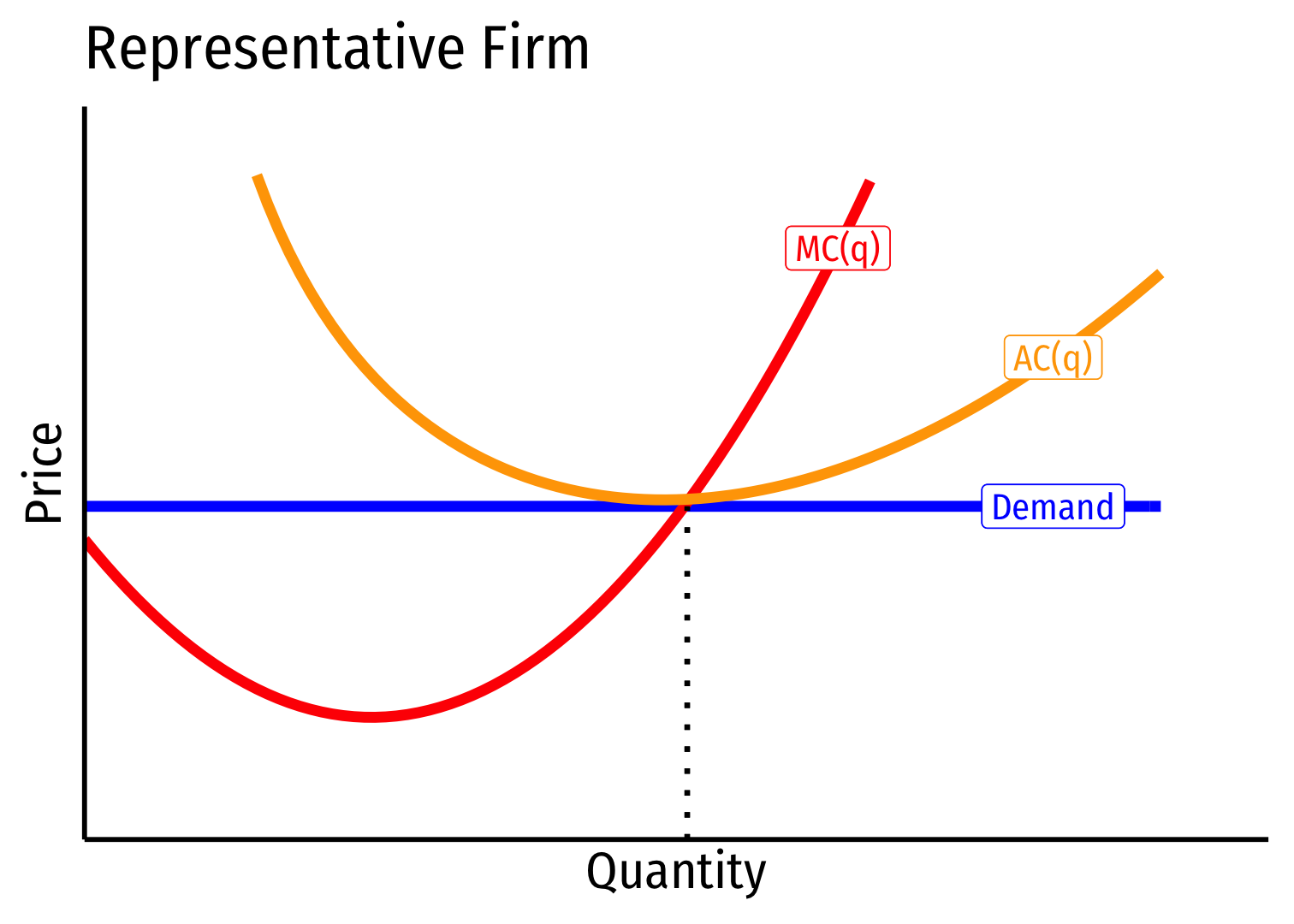

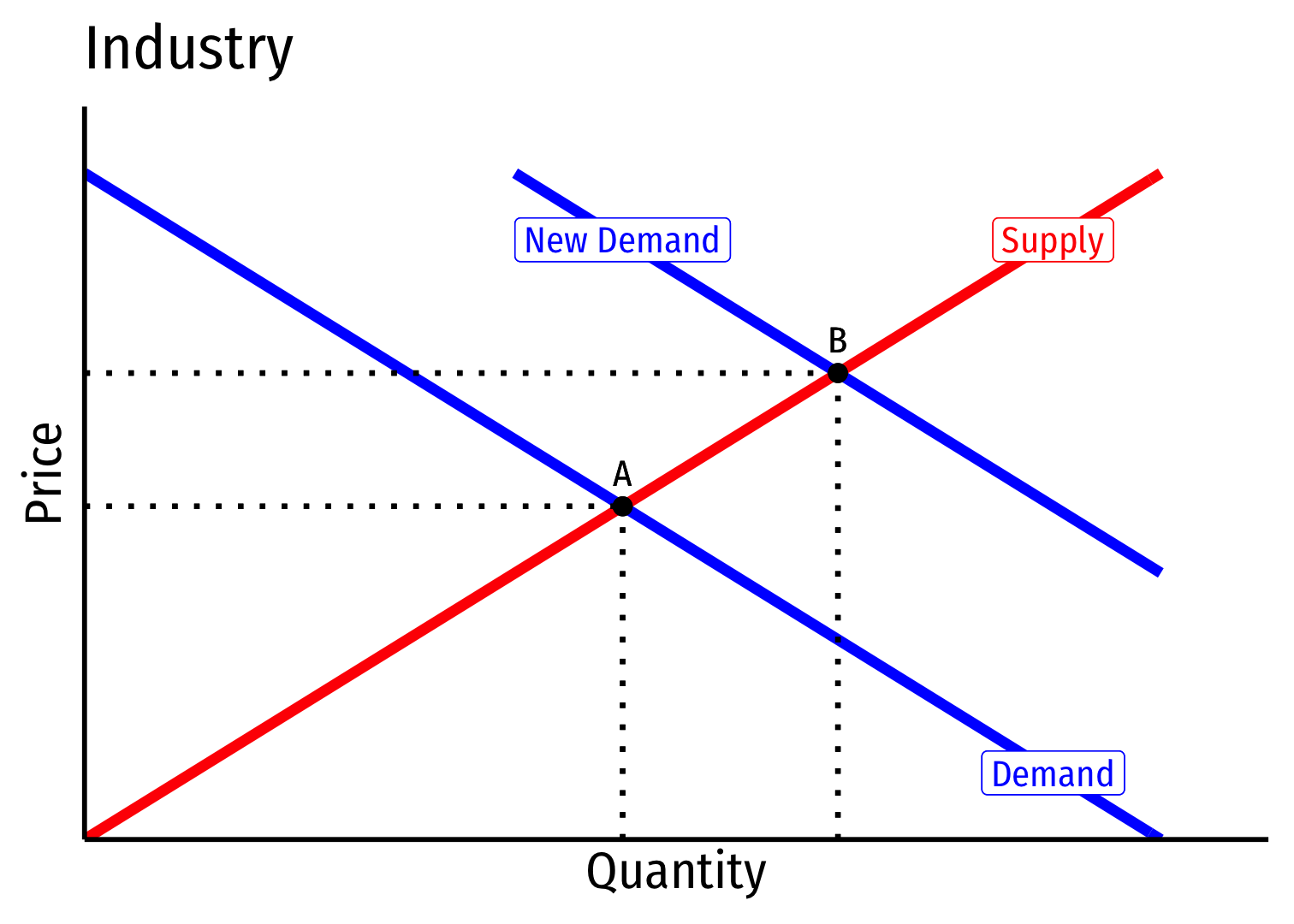

Constant Cost Industry (No External Economies) V

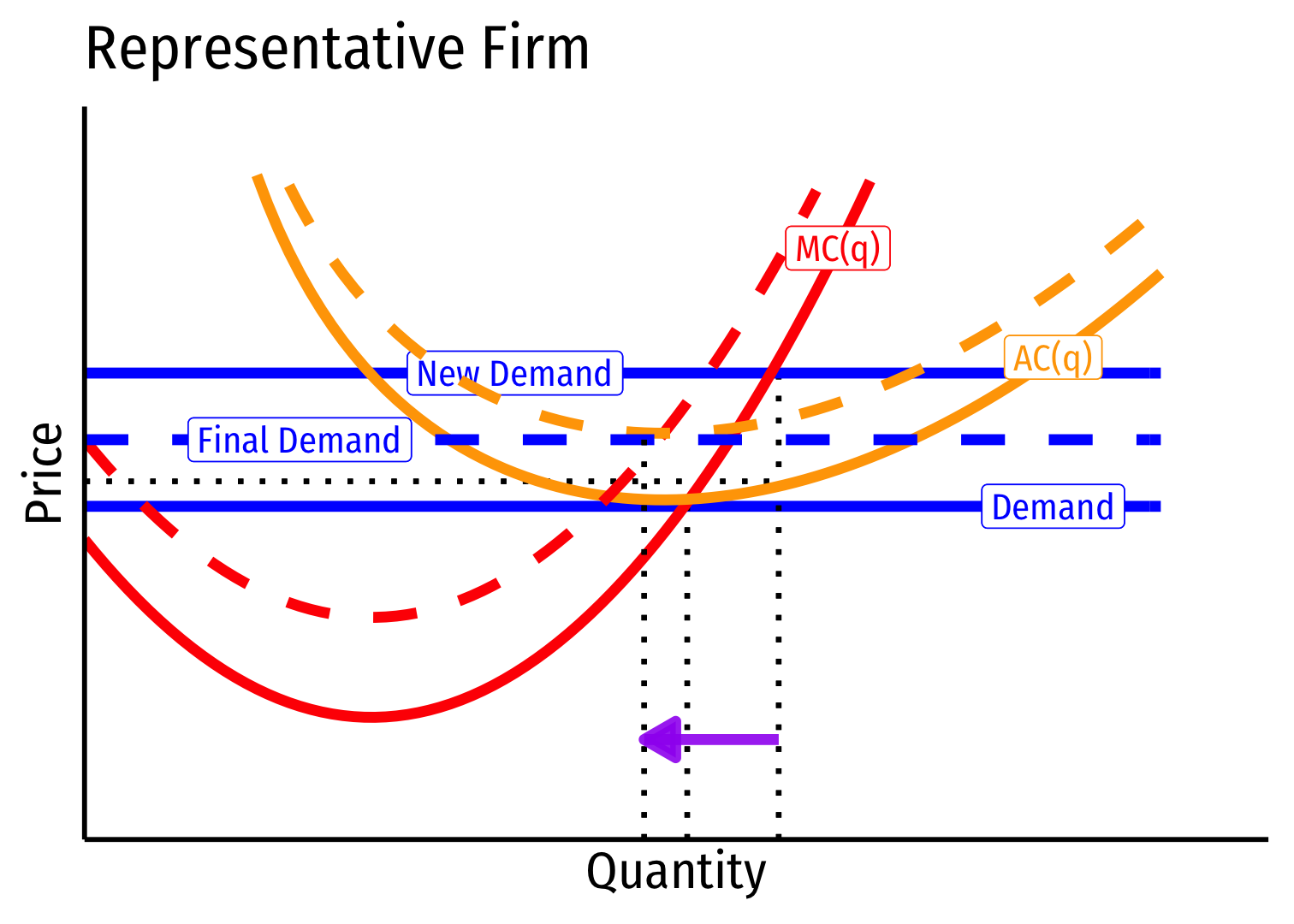

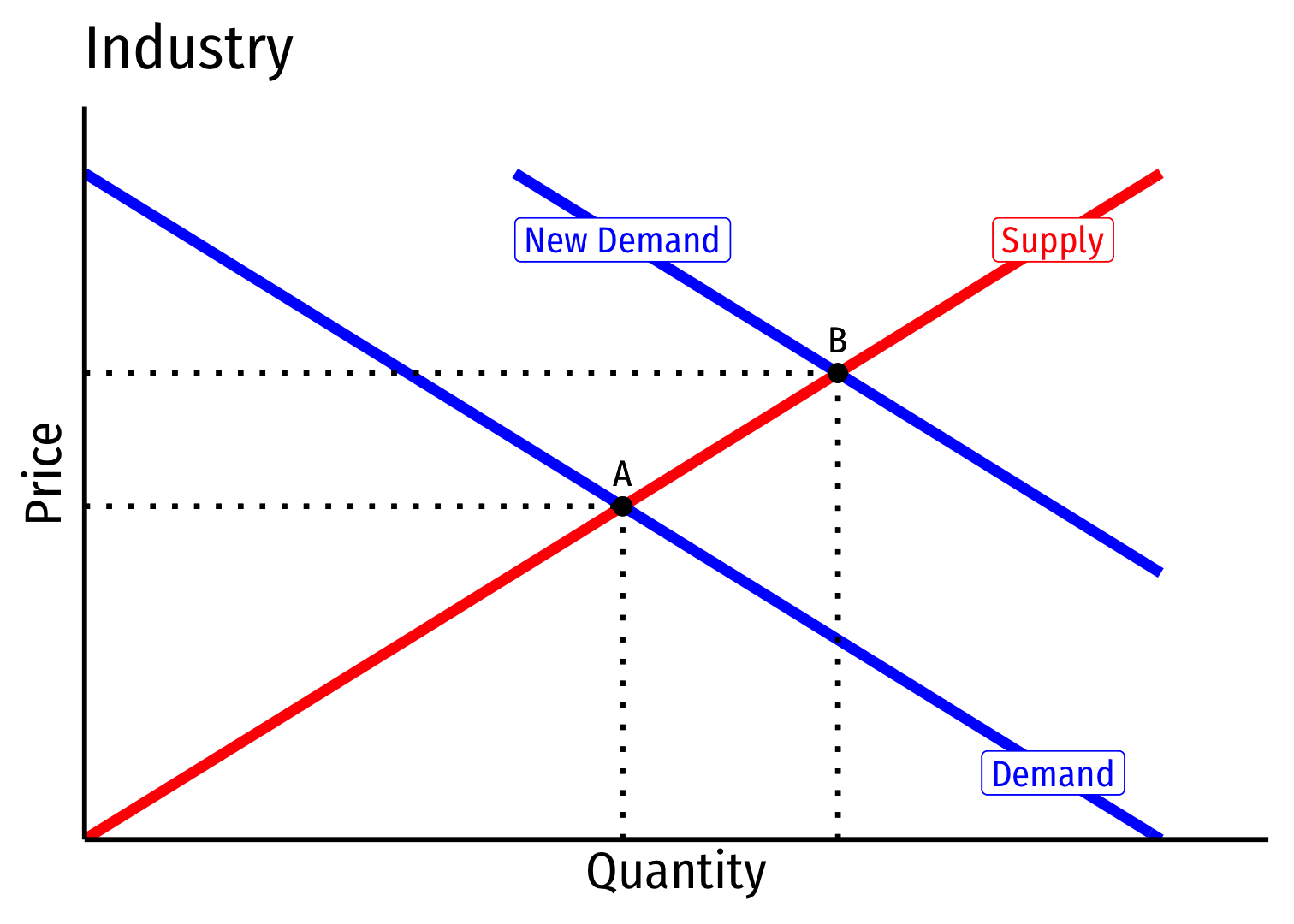

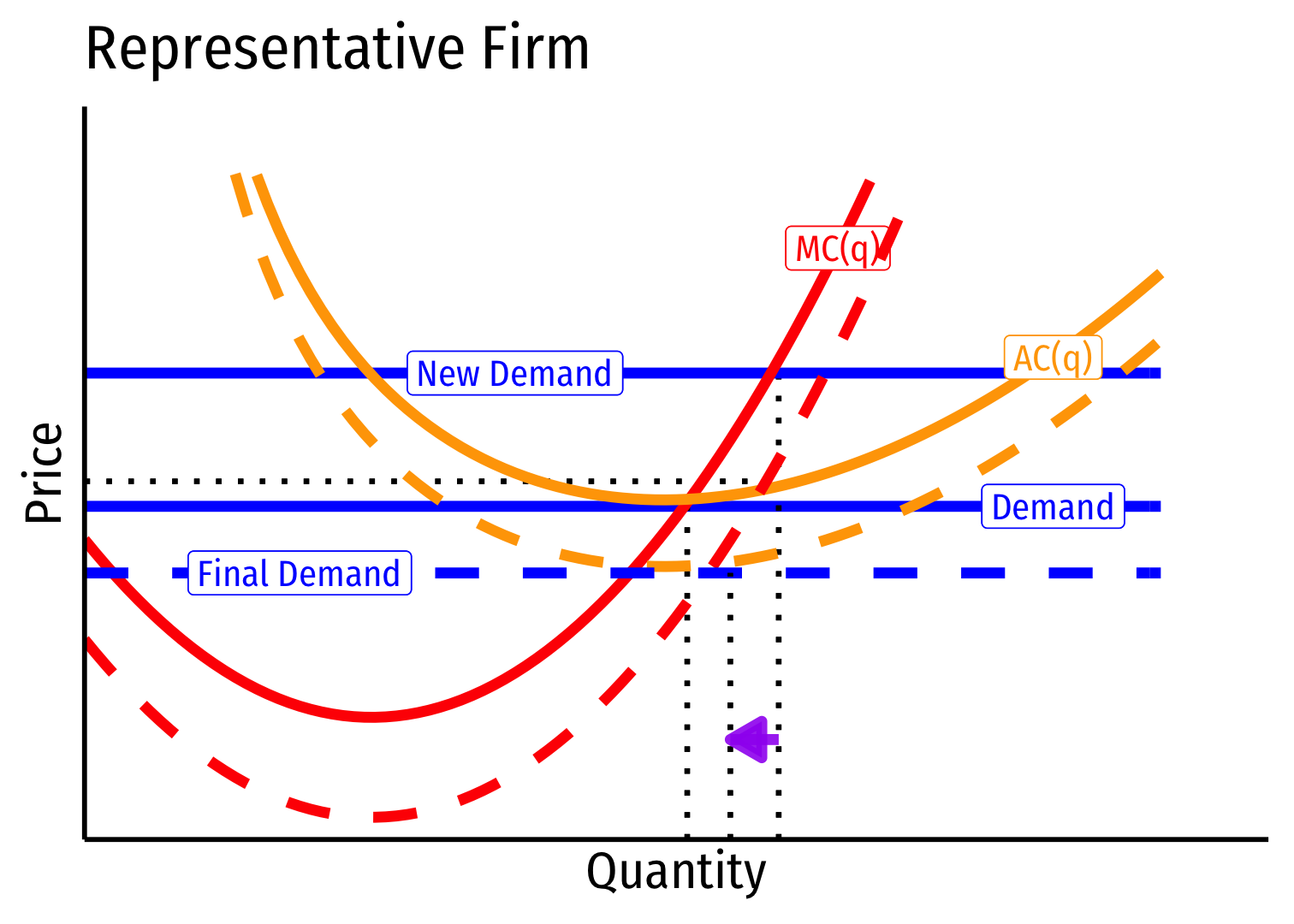

Long run (B→C): profit attracts entry ⟹ industry supply increases

No change in costs to firms in industry, firms enter until π=0 at p=AC(q)

Firms must charge original p∗, return to original q∗, earn π=0

Constant Cost Industry (No External Economies) VI

- Long Run Industry Supply is perfectly elastic

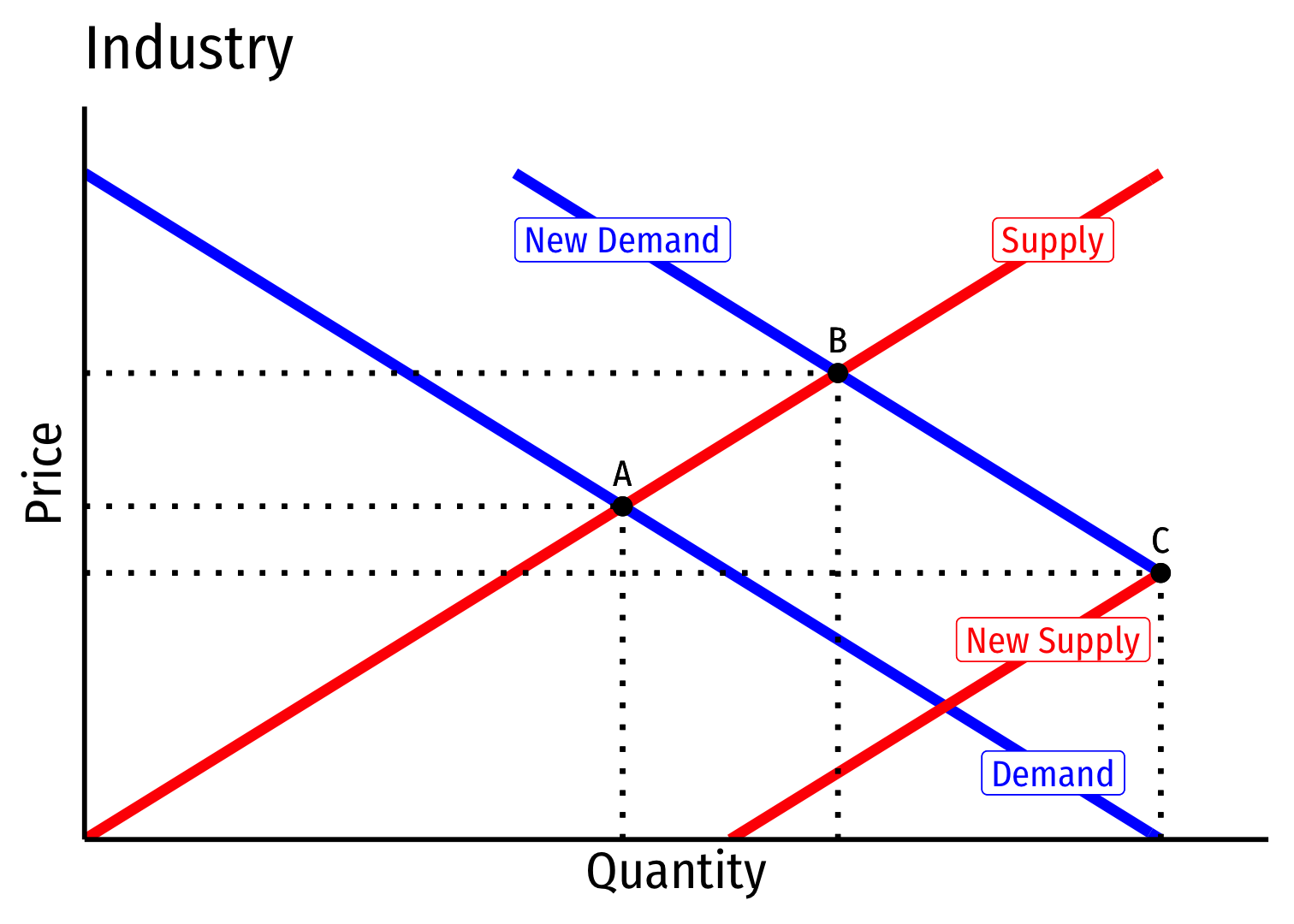

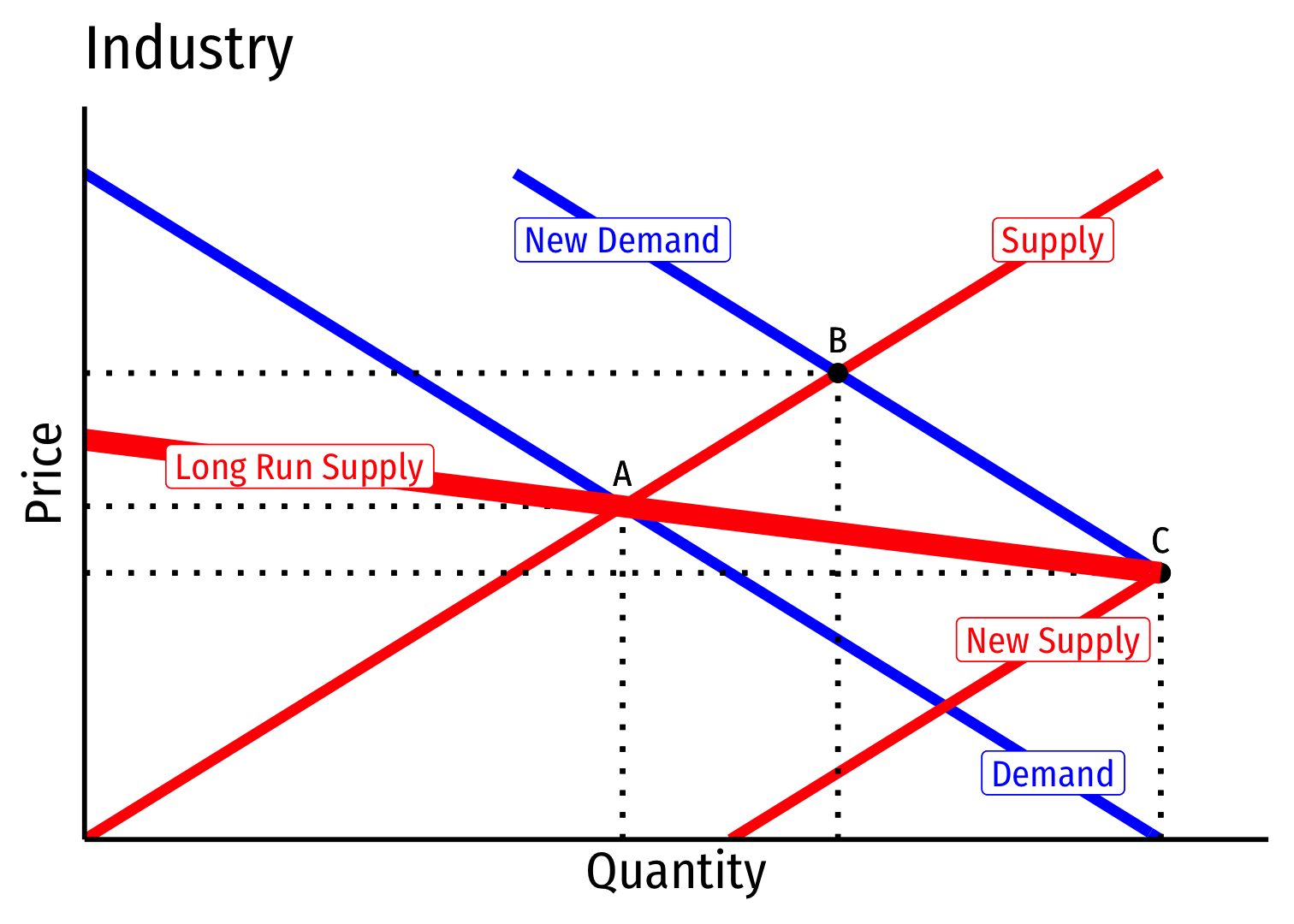

Increasing Cost Industry (External Diseconomies) I

Increasing cost industry has external _dis_economies, costs rise for all firms in the industry as industry output increases (firms enter & incumbents produce more)

An upward sloping long-run industry supply curve!

Determinants:

- Finding more resources in harder-to-reach places

- Diminishing marginal products

- Greater complexity and administrative costs at larger scales

Examples: oil, mining, particle physics

Increasing Cost Industry (External Diseconomies) II

- Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

Increasing Cost Industry (External Diseconomies) III

Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

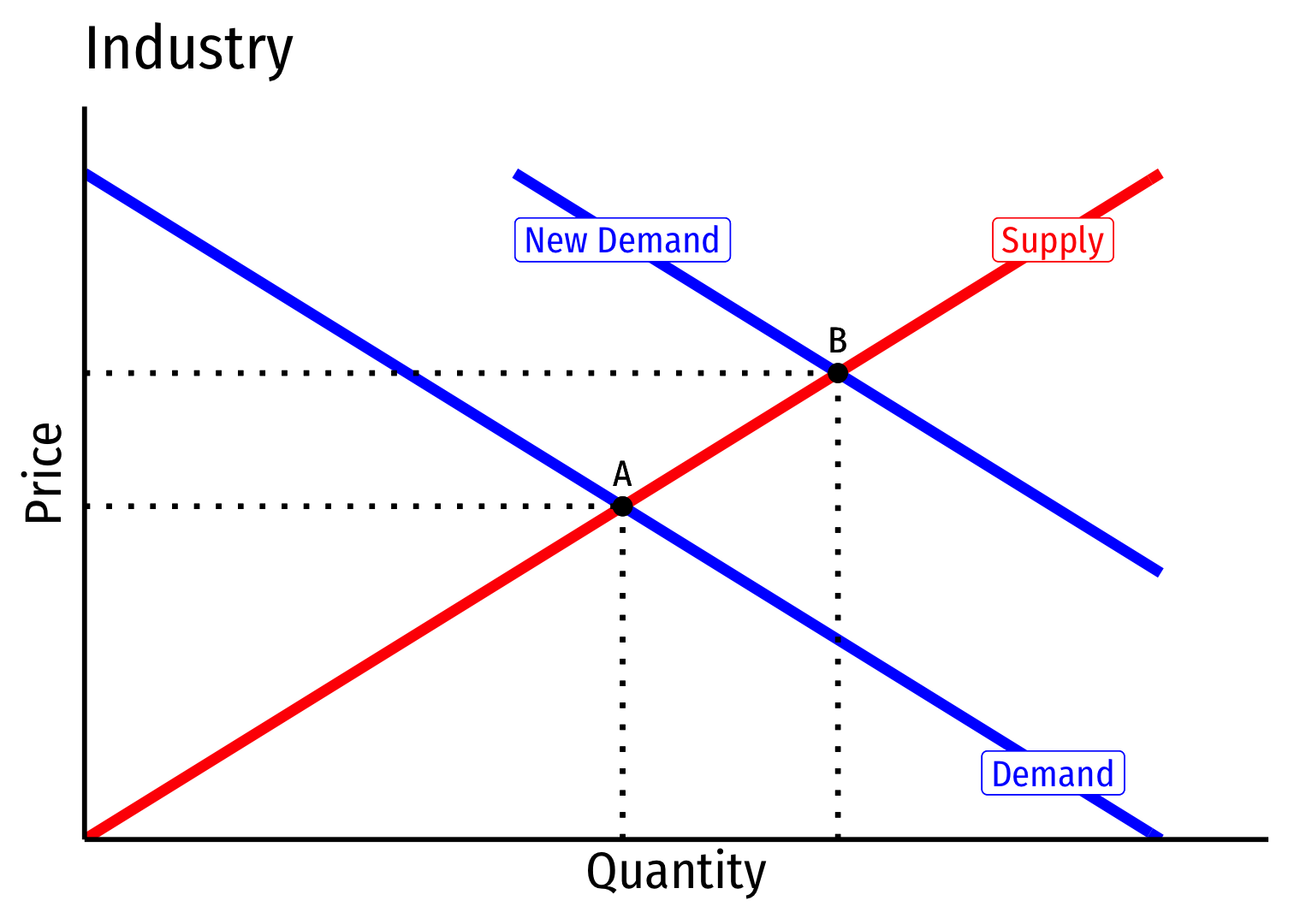

Exogenous increase in market demand

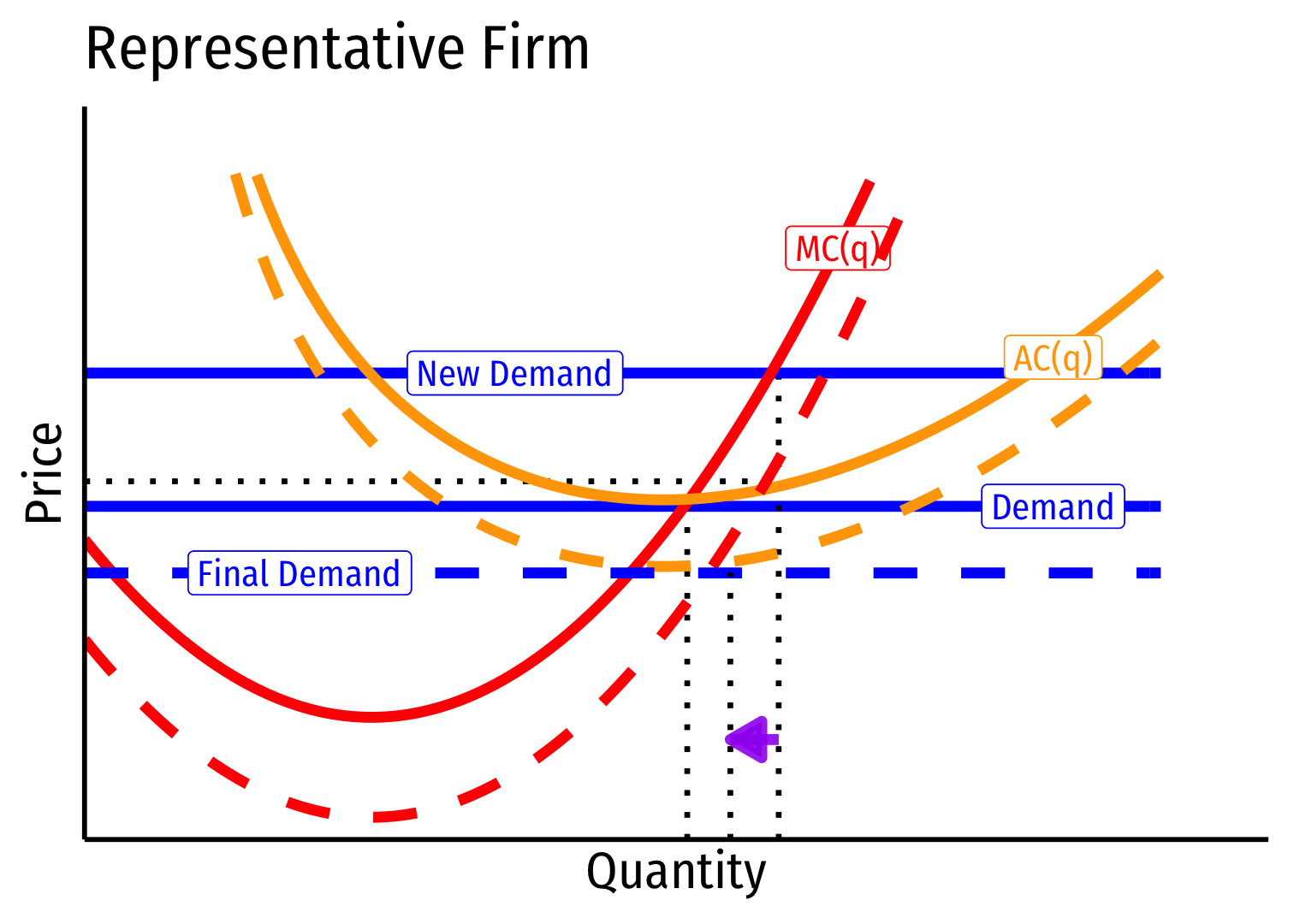

Increasing Cost Industry (External Diseconomies) IV

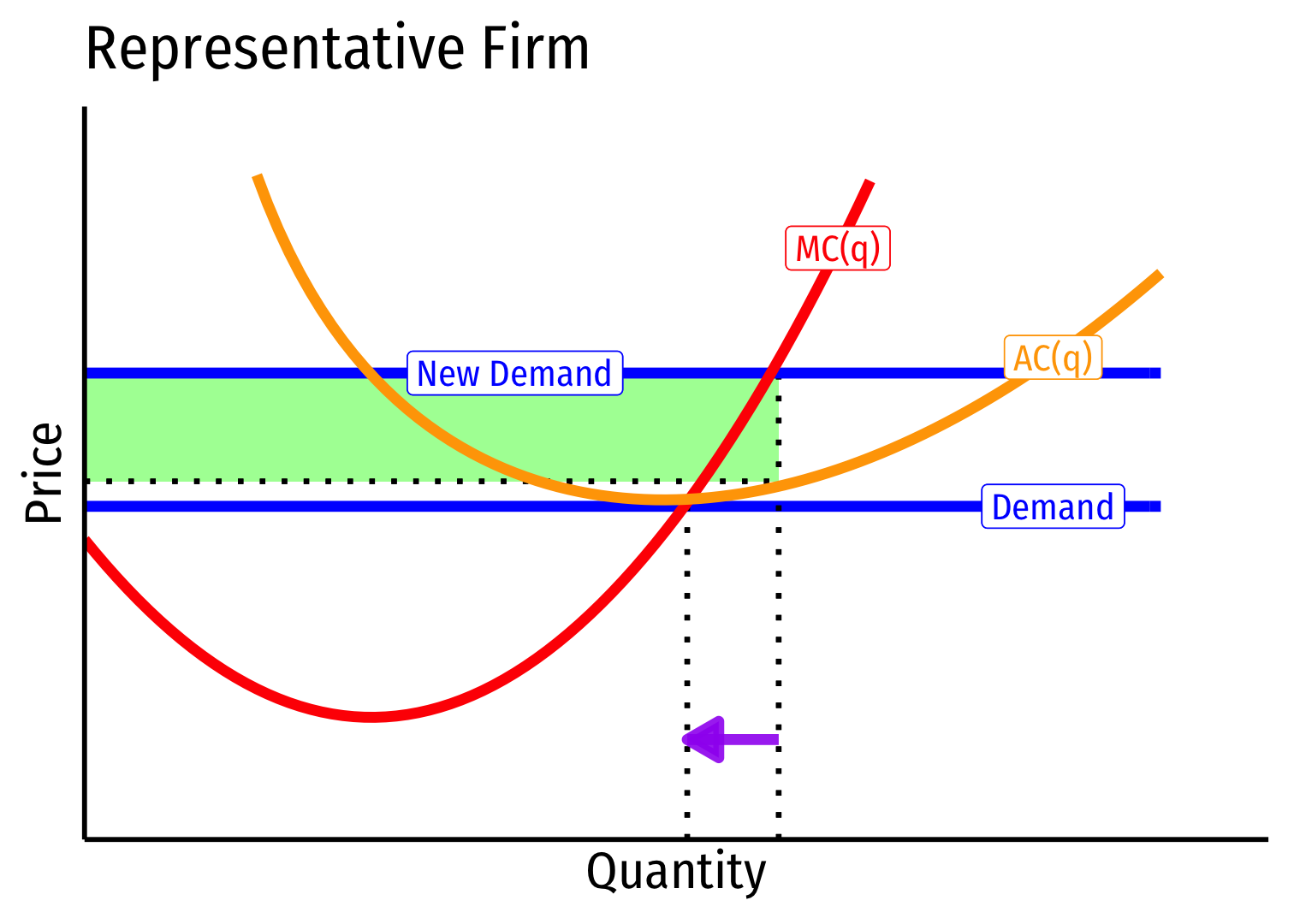

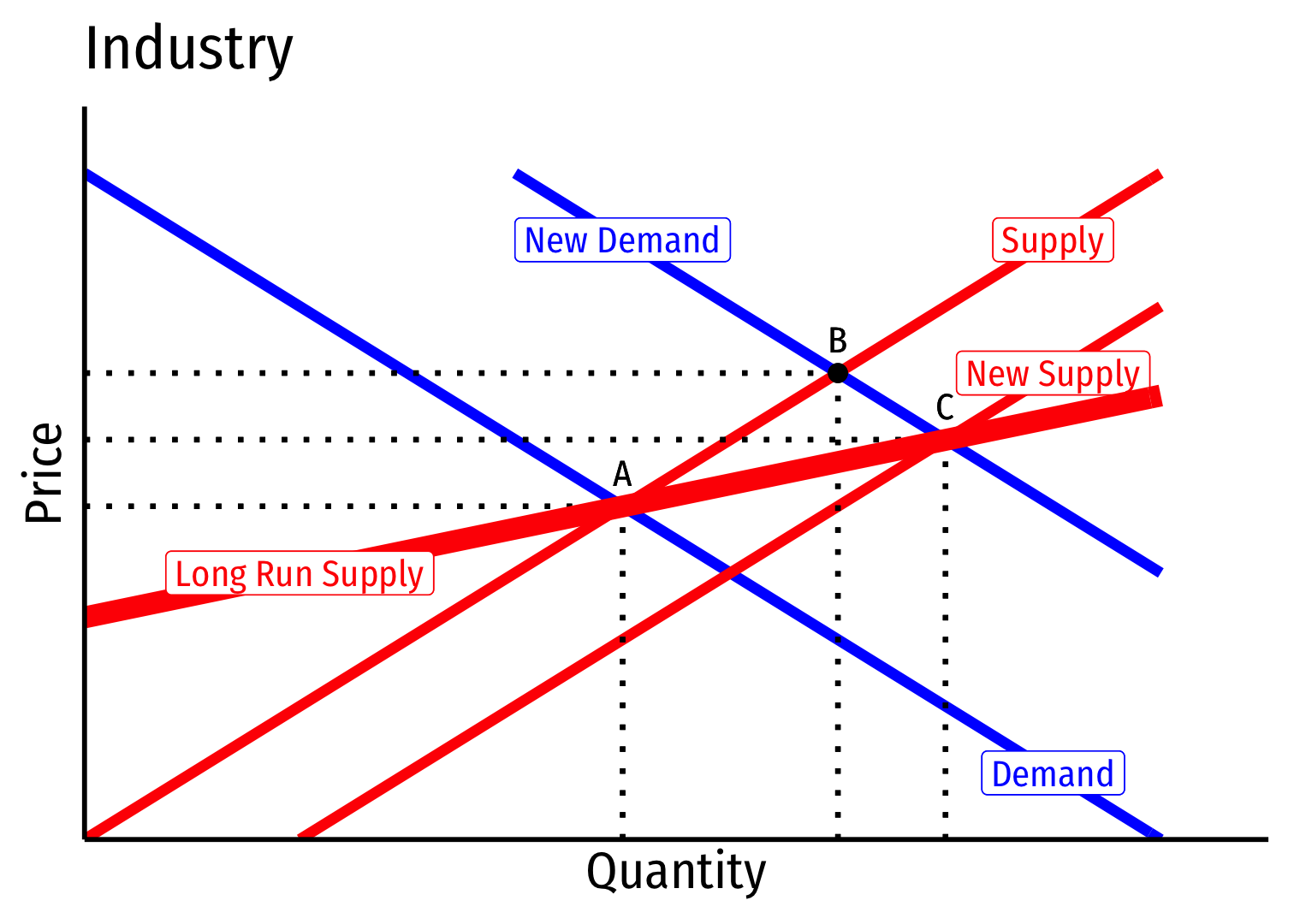

Short run (A→B): industry reaches new equilibrium

Firms charge higher p∗, produce more q∗, earn π

Increasing Cost Industry (External Diseconomies) V

Long run: profit attracts entry ⟹ industry supply will increase

But more production increases costs (MC,AC) for all firms in industry

Increasing Cost Industry (External Diseconomies) VI

Long run (B→C): firms enter until π=0 at p=AC(q)

Firms charge higher p∗, producer lower q∗, earn π=0

Increasing Cost Industry (External Diseconomies) VII

- Long run industry supply curve is upward sloping

Decreasing Cost Industry (External Economies) I

Decreasing cost industry has external economies, costs fall for all firms in the industry as industry output increases (firms enter & incumbents produce more)

A downward sloping long-run industry supply curve!

Determinants:

- High fixed costs, low marginal costs

- Economies of scale

Examples: geographic clusters, public utilities, infrastructure, entertainment

Tends towards "natural" monopoly

Decreasing Cost Industry (External Economies) II

- Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

Decreasing Cost Industry (External Economies) III

Industry equilibrium: firms earning normal π=0,p=MC(q)=AC(q)

Exogenous increase in market demand

Decreasing Cost Industry (External Economies) IV

Short run (A→B): industry reaches new equilibrium

Firms charge higher p∗, produce more q∗, earn π

Decreasing Cost Industry (External Economies) V

Long run: profit attracts entry ⟹ industry supply will increase

But more production lowers costs (MC,AC) for all firms in industry

Decreasing Cost Industry (External Economies) VI

Long run (B→C): firms enter until π=0 at p=AC(q)

Firms charge higher p∗, producer lower q∗, earn π=0

Decreasing Cost Industry (External Economies) VII

- Long run industry supply curve is downward sloping!